Table of Contents. Introduction

|

|

|

- Reginald Clarke

- 5 years ago

- Views:

Transcription

1 White Paper

2 Table of Contents Introduction 1. THE FUTURE OF THE DIGITAL ECONOMY AND ISLAMIC FINANCE 1.1 Overview of the development trends of Islamic finance 1.2 Comparison of the Islamic and Western economies 1.3 Islamic Cryptoeconomics 1.4 Conformity of the financing of projects on the cryptocurrency market to the rules of Islamic finance Problems of the Muslim Community Market Problems The importance of the Adab Solutions project for participants and its uniqueness 2. PROJECT 2.1 Objectives and mission of the project 2.2 Principles and values of the project 2.3 Solving key problems 3. ENSURING THE COMPLIANCE OF THE PRINCIPLES OF ISLAMIC FINANCE 3.1 Islamic governance model 3.2 Council on Islamic Finance 3.3 Charitable Foundation ADAB Charity 3.4 Jurisdiction of the project 4. ISLAMIC CRYPT EXCHANGE (FIRST ISLAMIC CRYPTO EXCHANGE) 4.1 Technical principles of the exchange Innovative and fast Matching Engine FICE Continuous development of FICE functionality Support for trading pairs in key cryptocurrencies Cross-platform trading clients and device support Multilingual technical support Trader rating 4.2 Generation of Exchange Revenue 4.3 Security of the Exchange

3 Table of Contents 5. ICO AND TOKEN ADAB 5.1 ADAB token 5.2 Conditions for ICO 5.3 Distribution of tokens 5.4 Forming the value of the token 5.5 Distribution of funds 6. PROMOTION OF THE PROJECT 6.1 Investor Relationships 6.2 Public Relations 6.3 ICO-Listing 6.4 Information support of the community. 7. THE ROADMAP OF THE PROJECT (ROADMAP) 8. BOARD OF ADVISORS 9. PROJECT TEAM

4 Introduction Introduction ADAB Solutions project developes the FICE - First Islamic Crypto Exchange, based on the principals of Islamik Finance. The purpose of the ADAB Solutions project is the creation of a cryptocurrency platform, exchange and services that comply with the norms of the Islamic Finance and operate on the principles of Islam. ADAB Solutions will create services based on the high moral and cultural values of Islam and will provide access to all users of crypto-economics. The principles and values of the project coincide with the principles on which Islamic finance are based on. The Islamic economic model today is one of the most dynamic areas of the modern economy, which is actively moving beyond the Muslim countries. 12% The growth rate of the Islamic Finance sector is 12% per year, moreover, the world market of Islamic Finance assets has exceeded 2 trillion and forecasted growth to 3.78 trillion dollars by The Islamic Ummah covers more than 120 countries in Europe, Western, Central, South and South-East Asia, and North Africa, which is a home for 22% of the world's population. ADAB Solutions has received few jurisdictions for the FICE project. This choice was made as a result of an analysis of the key advantages of jurisdiction. ADAB Solutions has 3 registrations, these are next: - ADAB Solutions - UAE, Umm Al Quwain - ADAB Solutions - UAE, Raz Al Khaimah - ADAB Solutions Group - Montenegro, Podgorica Also, ADAB Solutions Group is an official assignee of all obligations of the company in Raz Al Khaimah and Umm Al Quwain. 4 White Paper 1.0

.")

5 Introduction ADAB Solutions integrates the Islamic management model into the business management and business risk management system as an integral part of the company's management system, and ADAB Solutions will create the Shariah Advisory Board (Islamic Finance compliance Council). Islamic cryptocurrency platform ADAB Solutions implements the possibility of purchasing ADAB tokens by users during ICO. Estimated initial cost of the ADAB token is 0.1USD. The only release of ADAB tokens will occur during the ICO. ICO will be held from to % is the total share of tokens distributed among the community during pre-ico and TGE. Adab White Paper 1.0 5

6 Introduction Deflationary model of the ADAB token economy, based on using the token to access the services of the First Islamic Crypto Exchange and redemption of 10% of the FICE revenue, will significantly increase the attractiveness of participation in TGE ADAB, it is fair to reward participants, thanks to which the project could be implemented. The release of First Islamic Crypto Exchange is forecasted for a daily trading volume of about $ 146 million and a monthly turnover of $ 4.4 billion during the first and a half years of operation of the exchange. ADAB Solutions project will create a global infrastructure that operates on the principles of Islamic finance and the community that regulates the development of Islamic crypto-economics. ADAB Solutions will solve the problem of halal cryptocurrency transactions, providing access to the cryptocurrency market for the Muslim Ummah, which is 22% of the world population and manages Islamic financial assets with a forecasted volume of USD White Paper 1.0 6

7 The future of the digital economy and Islamic Finance The future of the digital economy and Islamic Finance 1.1 Overview of the development trends of Islamic finance Modern Islamic economic model is one of the most dynamic of the modern economy, and is actively moving beyond Muslim countries. Nowadays, Islamic finance is recognized by intergovernmental and international organizations as a form of financial intermediation, that has great potential to strengthen the links between financial institutions and the real economy. Understanding the essence and purpose of Islamic finance has significantly increased and was included in the agenda of G20 and OECD countries leaders meeting. The possibility for Islamic finance to expand the inclusiveness of financial services and achieve progress in general welfare are fully in line with the United Nations Global Sustainable Development Goals (SDGs). The International Monetary Fund (IMF) estimates that Islamic finance provides an opportunity for many IMF member countries to strengthen financial intermediation, increase the level of financial inclusion and attract investment for sustainable economic development. The World Bank (WB) considers Islamic finance an effective tool for financing world development, including non-muslim countries, which will solve poverty issues and promote global prosperity. The growth of the Islamic Finance sector stands at 12%, whilst the world market of Islamic Finance assets has exceeded USD. This is confirmed by the data from the "Towards Sustainability" report, which predicts the growth of the Islamic finance sector to reach up to 3.78 trillion dollars by White Paper 1.0

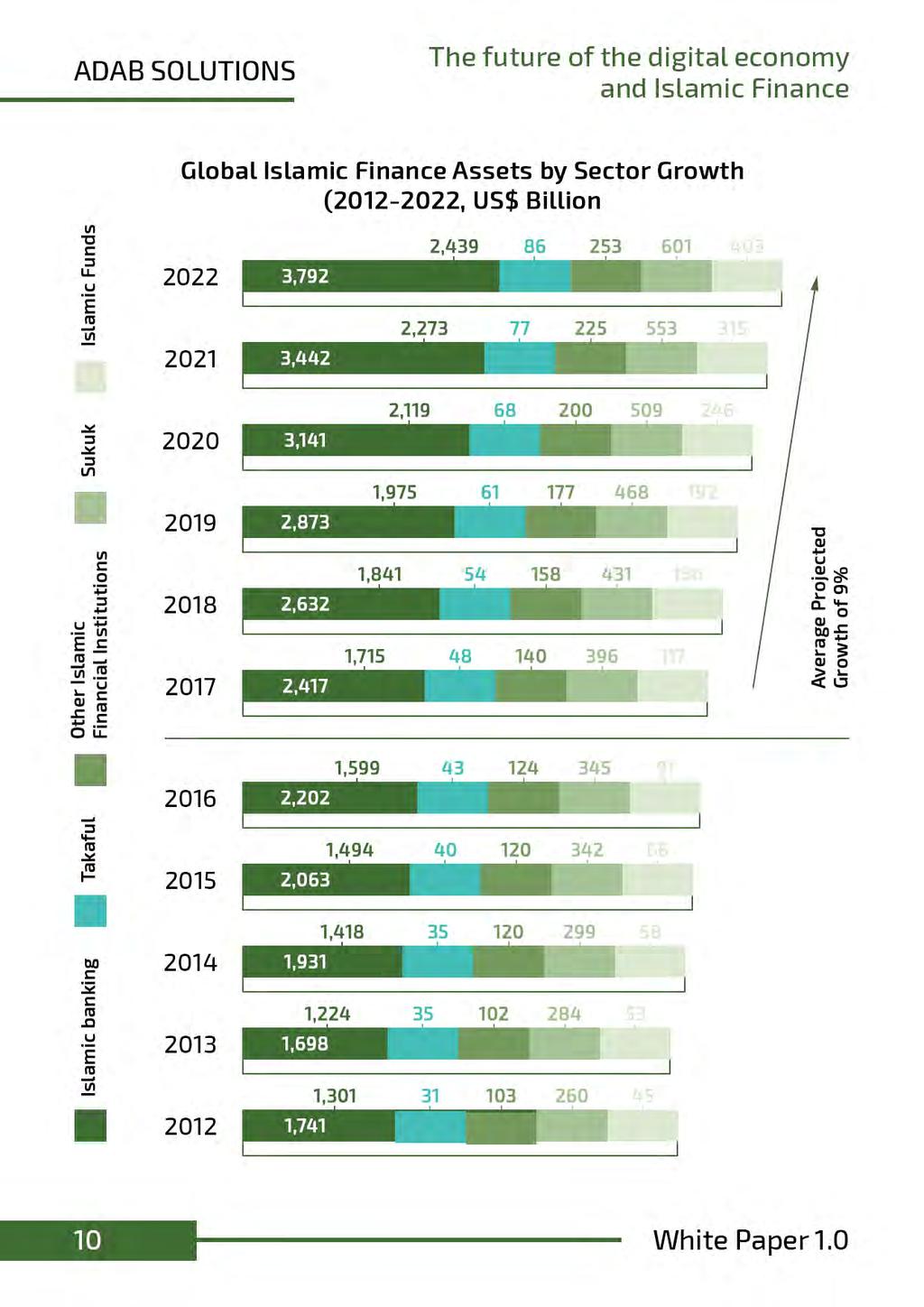

8 The future of the digital economy and Islamic Finance Islamic Finance Assets Growth ( ) Total Islamic Finance Assets (US$ Billion) 1,741 1,698 1,931 2,063 2,202 2,417 2,632 2,873 3,141 3,442 3,782 YEAR Projected growth The development of the industry will be driven by the increasing number of users of Islamic financial services, and greater funding. The Islamic finance industry is relatively well developed in the countries of Southeast Asia and the Middle East and demonstrates high growth potential in the countries of Europe, Africa and Central Asia. Prospective markets are the countries of South and North America and Australia. According to the Financial Stability Report IFSB (2016), the regional structure of Islamic finance is characterized by GCC dominance (39.9%); followed by a group of countries in the Middle East and North Africa (MENA, excluding GCC), which hold 32.2% of total Islamic financial assets. The largest contribution to the group of MENA countries is made by Iran, whose financial system fully complies with the Islamic principles of financing. The third place by asset sizes are occupied by the countries of Asia, with a share of 21.9%. The main contribution from this region is provided by the development of Islamic finance in Malaysia, Indonesia, Pakistan and Bangladesh (Table 1.1.). White Paper 1.0 8

9 The future of the digital economy and Islamic Finance The global industry of Islamic finance in terms of segments and regions (USD billion, 10 months of 2015). Types of assets (billion US dollars) Banks Sukuk Investment Funds Takaful Asia GCC (Gulf countries) MENA (excluding GCC) Africa (excluding the countries of North Africa) Other Total Source: Islamic Financial Services Industry Stability Report 2016, IFSB. Whilst in Islamic countries the Islamic economy is created with the support and initiated by the government, in non-muslim countries the emergence of Islamic financial institutions is driven by demand from the Muslim population for Shariah compliant financial services [cf. 6]. In 2018, Islamic banks, investment funds and insurance companies continue to be active in the western financial markets. Islamic financial institutions operate in the US, Italy, France, Sweden and other Western countries. The United States and other European countries, except Great Britain, have not yet received due attention or confidence from Islamic investors. In the list of the twenty leading countries in the world, Great Britain is the only non-muslim country with a high level of Islamic financial institutions assets. In the UK, there are six Islamic banks and an Islamic insurance company, the Islamic Bank of Great Britain (IBB) is well established, and within the traditional banks there are specialized units providing Islamic financial services. Globally there are more than 300 non-interest-based Islamic the annual growth rate of the sector is financial institutions in more than 50 countries; % 9 White Paper 1.0

10

11 The future of the digital economy and Islamic Finance According to the ISLAMIC FINANCE DEVELOPMENT 2017 report, it is expected that on average the growth rate of Islamic finance sector will be 9.5% per year, which significantly exceeds the growth rates of conventional financial institutions in the key regions of the world. 22% 22% of the world's population lives in Islamic countries. The Islamic Ummah covers more than 120 countries in Europe, West, Central, South and South-East Asia, and North Africa. In 35 countries, Muslims constitute the majority of the population, and in 28 countries Islam is a state religion these countries include Egypt, Saudi Arabia, Morocco, Kuwait, Iran, Iraq, and Pakistan, amongst others. Using an indicator based on the business climate of 73 countries, which include 57 countries of the Organization of Islamic Cooperation and 16 non-islamic countries with developed Islamic economies, Thomson Reuters identified the leaders in the development of Islamic economic systems. They are Malaysia, Pakistan, Singapore, UAE, Kuwait, Brunei, Bahrain, Qatar, Sudan, Saudi Arabia, Jordan, Iran, Oman, and Indonesia. It is worth mentioning that Islamic finance and the halal food industry accounted for 45% and 35% respectively of the total economy for these countries. A positive trend in the development of the Islamic financial and economic system indicates an opportunity for further growth. According to the forecasts, Islamic the asset management sector has the highest potential for growth. Islamic investment and hedge funds will also potentially grow, as global financial investors direct their attention to investment opportunities in the key growing markets of Islamic countries. White Paper

12 The future of the digital economy and Islamic Finance Comparison of the Islamic and Western economies It can be argued that the Islamic economy, now has a global influence. At the same time, it is necessary to realize that when we talk about the "Islamic economy", we are talking about the origin of the ideas that formed the basis of this concept. The concept of the "Islamic economy" does not in itself contradict the classical Western economy; and does not form any specific laws of economic development. The main differences are in the basic values of the economy. The primary sources of Shariah - the Quran and the Sunnah - regulate the basic issues related to economic activity, based on this, Muslim scholars and economists formulated the key provisions of the Islamic economic model. The term "Islamic Finance" includes a wide range of financial products and services. In most cases, they have some similarities to traditional financial services, since their main goal is to promote investment by capital owners, and spark the interest of capital users. 12

13 The future of the digital economy and Islamic Finance Islamic Finance complies with Shariah law. This causes the differences between the conventional and the Islamic principles of financing. According to general economic laws, Islamic Finance developed based on Shariah law. It should be understood that Islamic finance is not a purely religious phenomenon. In some countries, Islamic banking products are also popular with the non-muslim population. According to Sheikh Saleh Kamel, a pioneer of Islamic finance - Islamic finance is based on three pillars: Profit sharing, as an alternative to interest Commitment to moral principles and socially responsible investments for the benefit of the whole community Adding the real value to trading operations The general restrictions governing Islamic Finance can be defined as follows: Financial transactions cannot be based on speculation; Financial transactions cannot be based on obtaining interest on capital; Financial transactions cannot be related to activities prohibited by the Shari'ah, including gambling, pork products, alcohol and pornography; The risks of any financial transaction should be shared by all involved parties. White Paper

14 The future of the digital economy and Islamic Finance The table below outlines the fundamental differences in the economic principles of the Islamic and Western economic systems: Islamic economic principles Western economic principles The source of Islamic economic principles is the Quran and Sunnah A holistic view of the world, the perception of finance and economics as part of Creation Individual property and capital are relative Economic mechanisms are based on public interest (Maslaha) Competition in business is subject to the norms of Shariah Accepting profits only from activities recognized as permitted (Halal) The government and the Islamic Supervisory Board act as an observer, controller and fair arbitrator in economic activities The source of Western economic principles are human experience and theories A secular worldview Individual property and money are absolute Market mechanisms are based on individual benefits Competition in business is free, allowing the creation of monopolies Aspiration to profit without any moral restrictions Government as a neutral passive spectator in economic activity Unallocated distribution of income through taxes Fair distribution of income - Zakat 14 White Paper 1.0

15 The future of the digital economy and Islamic Finance In the 21st century, the Islamic economic model overcomes the shortcomings of the capitalist and conventional economic systems that dominated in the 20th century. This is reflected in the fact that in the Islamic economy a golden mean has been found between the absolutizing of private property under capitalism, and it s almost complete negation in conventional forms of the economy. 1.3 Islamic Crypto economics Islamic crypto-economic systems can be characterized as a set of financial mechanisms that allow individuals to carry out investment activities without violating the basic principles of the Sharia. According to the ISLAMIC FINANCE DEVELOPMENT report 2017, the cryptocurrency economy is one of the key areas of innovation in the field of Islamic finance. Islamic investors are aware of the prospects of the cryptocurrency economy. This interest was expressed in the creation of cryptocurrency projects in Islamic countries, in particular, crypto-exchange sites were established in Indonesia, Malaysia and the UAE. BitOasis, based in the UAE, offers its services in Kuwait, Bahrain and Saudi Arabia. In the Southeast Asia region, Bitcoin Indonesia and Coinbox in Malaysia have been established to offer Bitcoin related services. At the same time, it is important for the development of the cryptocurrency economy to understand whether cryptocurrency is Halal for Muslims or not. The table below outlines the main approaches to the admissibility of using crypto currency: HALAL 1. Researchers from the Indonesian company BlossomFinance came to the conclusion that the first crypto currency is compliant with all Sharia law [7]. 2. The founder of the BlossomFinance system in Indonesia, Muslim Matthew Martin believes that as a payment system, bitcoin is halal (permissible). In fact, Bitcoin goes beyond what the banking system offers, in which there is no guarantee that the initiator owns the assets. Bitcoin guarantees with mathematical precision that the initiator of the transaction owns the underlying assets. "Ordinary banks operate using a partial reservation system, which is banned in Islam," said the founder of the fintech platform. White Paper

16 The future of the digital economy and Islamic Finance Matthew believes that, in comparison with conventional fiat currencies, bitcoin is more halal, justifying it by the fact that fiat currency is based on usury, which is forbidden by the Shari'ah. 3. Sheikh Dr. Adnan Al-Zarani (former chairman of the Shari'ah Supervisory Board of Al-Jazeera Bank): "Crypto currency is one of the types of currencies / money that emerged as a result of the process of creating and developing money. In other words, at first the ego was an ordinary barter. Then gold and silver coins, and then paper money. Now virtual money, which are cryptocurrencies. And this is normal." 4. Mufti AbdulKadar Barakatulla (member of the Shariah Committee in Al-Ryan Bank) "I am convinced that cryptocurrencies can be an effective tool for the further development of Islamic finance." 5. Operations with bitcoins and other crypto currency from the point of view of Islam are inappropriate. This was stated in the Office of Religious Affairs of Turkey. "The purchase and sale of crypto currency is inappropriate from the religious point of view, because these operations are open to speculation and they can be easily used for illegal purposes, such as money laundering. Cryptocurrencies are also far from state audit and supervision " HARAM 1. Operations with bitcoins and other crypto currency from the point of view of Islam are inappropriate. This was stated in the Office of Religious Affairs of Turkey. "The purchase and sale of crypto currency is inappropriate from the religious point of view, because these operations are open to speculation and they can be easily used for illegal purposes, such as money laundering. Cryptocurrencies are also far from state audit and supervision". 2. The fatwa of Egypt's supreme mufti Shauka Allam on the prohibition of bitcoin for Muslims. In the fatwa of Mufti Allam, it is stated that bitcoin "is not an acceptable means for monetary exchange, and therefore cannot be used in a trade." "Bitcoin is banned from the standpoint of the principles of the Shariah, as it harms individuals, groups of people and institutions," the fatwa says in the text. 16 White Paper 1.0

17 The future of the digital economy and Islamic Finance 3. Sheikh Imran Hussain: any currency that does not have its own intrinsic value cannot be considered valid. Therefore, only gold or silver money can meet the Shariah criteria. 4. Prof. Ahmed KamelMidin Measure: in order for a digital currency to be accepted in the Islamic finance industry, it should have some value, and electronic currencies should be redeemed, for example, with gold. Otherwise it's unfair. 5. The AAOIFI Shariah financial standards do not yet cover this topic, although it is possible that in the next 2-3 years the Shariah standard on cryptocurrency will be developed. NEUTRAL RELATIONSHIP 1. The AAOIFI Shariah financial standards do not yet cover this topic, although possibly the Shariah standard on crypto currency will be developed in the next 2-3 years. 2. Fatwa of Monter Kahf on crypto currency. "Let's now look at the Shariah aspect. Like any other currency, it's money inside your community and exchanging them for other currencies, of course, is subject, in my opinion, to the same conditions of currency exchange that exist in charite. Namely: 1) there must be a delivery (transfer) of both exchange items, there should not be futures; 2) there should not be speculation in the currency, that is, people who exchange the currency should have the purpose of buying or selling, in addition to currency for the sake of currency (that is, the goal should be to buy it to use or sell, because you received it, but you need other currency). 3. From the Shariah point of view, bitcoin operations carry the elements of Gharar (uncertainty of the transaction) and Maysir (high risk inherent in gambling). In Islamic law, there is also the notion that money is printed only by the State, and in the case of mining, this concept does not work. At present, according to the crypto currency, the Shariah standard has not been developed, since it is also impossible to forbid them as haraam. 4. Fatwa on the site Q: What is the view of Shariah on the acquisition of bitcoins? A: Despite the presence of unwanted aspects in electronic money, such as strong volatility and speculation, we still have no right to prohibit them, as the aforementioned negative indicators in most cases are already present in the markets. White Paper

18 The future of the digital economy and Islamic Finance Q: What is the view of Sharia for buying and selling electronic money (bitcoins), and also for mining? A: Anyone who has acquired electronic money in a legitimate way, can use them, it is permissible. The digital currency differs from paper money or ordinary coins. But the purchase of these electronic money is regarded as a full-fledged currency exchange. Summarizing the above, we can conclude that the cryptocurrency economic system is not Haram or Halal in and of itself, it is a technology that can be turned to the benefit of Muslims, and in this case, will become Halal. However, violating the norms of the Shariah through any action or technology is clearly Haram. In order to make ADAB Solutions cryptocurrency project Halal, it is planned to implement the following measures: 1. The entrepreneurial efforts of the organizers and their work will be put into the development of the project. According to the norms of Islamic ethics, it is right that the source of any wealth is its own labor, and the entrepreneurial efforts of its owner. 2. The first Islamic Crypto Exchange will completely exclude the possibility of speculative transactions, margin trading and operations that do not correspond to Sharia. This will exclude the Gharar, Maisir and Ribu from the work of the Exchange. 3. ADAB Solutions will complete and pass Islamic expert assessment on compliance with Sharia law. 4. ADAB Solutions organizes the Shariah Supervisory Board under the First Islamic Crypto Exchange. 5. ADAB Solutions will adhere to documents and procedures, prepared on the basis of a serious analysis, that regulate the company's work with crypto assets in accordance with the norms of Sharia. 18 White Paper 1.0

19 The future of the digital economy and Islamic Finance 1.4 Conformity of the financing of projects on the cryptocurrency market to the rules of Islamic finance For a correct understanding of how Islam and the principles of Islamic finance can relate to cryptocurrencies, it is necessary to understand when and how Islamic economic model works and are approved by the Shariah rules: - ISLAMIC STOCK MARKETS - CROWDFUNDING AS A WAY OF FINANCING BUSINESS IN SHARIA There are many Islamic stock exchanges in the world, including the Kuala Lumpur Stock Exchange, the Dubai Stock Exchange, and the Khartoum Stock Exchange. In addition, there are a number of Islamic stock indices, such as the S & P 500 Sharia Index, S & P Europe 350 Shariah, KHARTOUM Index, Kuala Lumpur Syariah Index (KLSI) and many others. The study "Islamic norms for stock screening A comparison between the Kuala Lumpur Stock Exchange Islamic Index and the Dow Jones Islamic Market Index" states that these exchanges are based on the basic principles of Islam, such as the prohibition of usury, compliance with Shariah law, prohibition of speculation, and risk sharing. In Malaysia, KLSESI, an important ICM product, was introduced in 1997 to enable Muslim investors to participate in equity investments in accordance with the principles of the Shariah. As of October 26, 2006, 642 of the 811 companies traded on the exchange were approved by SAC SC as eligible securities. According to the SC, SAC applied standard criteria as guidelines to determine whether the main assets of companies listed in KLSE are admissible for investment under the Shariah. Activities are considered to be prohibited if: 1. Operations are based on riba (percentages) such as commercial and trade banks, and financial companies. 2. Operations include gambling. 3. Activities include the production and / or sale of prohibited products (haram), such as liqueur, or pork and animal meat not slaughtered by Shariah rules. 4. Operations contain elements of Gharar (uncertainty), as in conventional insurance companies. White Paper

to the Muslim Ummah and the country, while the haram (illegal) element is avoided or very small.")

20 The future of the digital economy and Islamic Finance For companies, whose activities consist of both permissible and unacceptable elements, SAC has established the following additional criteria: 5. The main activities of companies should not conflict with the principles of the Shariah, set out in the four above criteria. In addition, the proportion of illegal (haram) elements should be very small in comparison with the main activities. 6. Public perception or company image should be good and beneficial (profitable in general) to the Muslim Ummah and the country, while the haram (illegal) element is avoided or very small. Summarizing the above, we can conclude that the cryptocurrency economic system is not haraam or halal in and of itself, it is a technology that can be used for the benefit of Muslims, and will become, in this case, halal. However, violating the norms of the Shariah through any action or technology is unequivocally haram. In order for ADAB Solutions crypto currency project to be Halal, it is planned to implement the following measures: 1. The entrepreneurial efforts of the organizers and their work will be put into the development of the project. According to the norms of Islamic ethics, it is right that the source of any wealth is its own labor, and the entrepreneurial efforts of its owner. 2. The first Islamic Crypto Exchange will completely exclude the possibility of speculative transactions, margin trading and operations that do not correspond to Sharia. This will exclude the Gharar, Maisir and Ribu from the work of the Exchange. 3. ADAB Solutions will complete and pass Islamic expert assessment on compliance with Sharia law. 4. ADAB Solutions organizes the Shariah Supervisory Board under the First Islamic Crypto Exchange. 5. ADAB Solutions will adhere to documents and procedures, prepared on the basis of a serious analysis, that regulate the company's work with crypto assets in accordance with the norms of Sharia. 6. Public perception or company image should be good. 20 White Paper 1.0

of the Muslim Ummah and the country, while the haram (illegal) element is absent or very small.")

21 The future of the digital economy and Islamic Finance 6. Public perception or company image should be good. 7. The main activity of the company is important and is Maslahah (profitable in general) of the Muslim Ummah and the country, while the haram (illegal) element is absent or very small. The main activities are connected, combining the benefits of social development and investment opportunities based on the distribution of profits and losses for a wide range of entrepreneurs and investors. 8. The level of interest (income) received from fixed deposits in conventional financial institutions and other investments in interest-bearing accounts do not exceed the levels established by SAC. The development of the stock market is a good indicator of a country's economic development, as in Malaysia s case. The stock market is a suitable place for Islamic investors to avoid the threat of inflation and at the same time is an indicator of the development of the nation from an economic standpoint. For example, in Malaysia, the KLSI index, consisting of shares of Shariah-compliant companies and admitted to trading by the Shariah Advisory Board of the Securities Commission, is intrinsically connected with the economic growth of Malaysia. The study, The Macroeconomic Variables and the Malaysian Islamic Stock Market: A Time Series Analysis, examines the relationship between Malaysia's GDP growth, and the growth of major stock indexes. The correlation is quite significant and shows that the growth of indices causes GDP growth, while decrease in indices cause a drop-in GDP. Thus, investments from the Shariah point of view are quite acceptable, but with certain limitations. The presence of large international experience and practice clearly proves this. The World Bank-Islamic Development Bank Policy Report "LEVERAGING ISLAMIC FINANCE FOR SMALL AND MEDIUM ENTERPRISES (SMEs)", published in October 2015, details how crowd financing is a means of financing business in accordance with the norms of the Sharia. White Paper

22 The future of the digital economy and Islamic Finance The authors distinguish the following types of crowdfunding: Crowdfunding on the basis of donations: Usually sponsors support the initiative through donations - no future compensation is expected. Crowdfunding based on remuneration: Sponsors receive tokens for supporting the initiative, or samples of products or services being developed. Reward based crowdfunding is an excellent online option to pre-sell products and use these revenues to produce goods and services. Crowdfunding on the basis of credit: While the first two types are more philanthropic by nature, credit-based crowdfunding is an investment tool by which crowd investors provide support loans to start-ups or small businesses to make a profit in the form of interest payments. Equity crowdfunding: Crowdfunding on the basis of credit. In this scenario crowd-investors support start-ups or small businesses for financial gain. As part of the equity investment, investors receive shares in the enterprise, so this can be considered as a profit and loss sharing agreement. This method of crowdfunding has parallels with the venture capital industry. From the listed forms of crowdfunding, only crowdfunding on the basis of credit does not comply with Islamic law. The other forms of crowdfunding are fully consistent with Shariah and are actively used in Islamic finance. Let's look at a few examples of crowdfunding platforms working on the basis of Islamic law: Liwwa: an electronic crowd-hosting platform based in Jordan, was launched in September It helps small businesses meet capital needs by raising funds from a variety of investors, subsequently paying back the amount received by sharing the profit in the form of monthly payments or installments. 22 White Paper 1.0

23 The future of the digital economy and Islamic Finance Shekra: crowdfunding platform, founded in Egypt, was launched in November It solves the problem of financing shortages for start-ups that are too large for incubators, too small for venture capital funds and too risky for banks. Financing start-ups ranges from $ 20,000 to $ 200,000. To meet the needs of both start-ups and small and medium-sized enterprises using the Shekra platform, companies can receive equity financing in the form of Musharaka and a reduced Musharaka. Shekra won the Sheik Mohammed Bin Rashid Al Maktoum s Islamic Economy Award in the United Arab Emirates and the Ethical Financial Initiative Award of Thomson Reuters and Islamic Bank of Abu Dhabi. From the point of view of Islamic finance, crowd equity is a significant opportunity to realize the basic expectations of Islamic finance. This is achieved by combining the benefits of social development and investment opportunities, based on the distribution of profits and losses for a wide range of entrepreneurs and investors. Financing of promising start-ups and small businesses around the world should be based on alternative sources of financing. Innovative financial services increase the availability of financing to meet the needs of entrepreneurs around the world and drive technological developments. White Paper

, as required by the")

24 The future of the digital economy and Islamic Finance In the last few years, innovative financial services have become increasingly important. The advantages of crowdfunding from the Islamic finance perspective include the following: Operates based on the distribution of profits and losses (Musharaka or Mudaraba), as required by the principles of Islamic finance Provides access to capital for a wide range of entrepreneurs, thereby reducing the funding gap Opens a new asset class for small and medium-sized investors Minimizes risk by dividing capital into several start-ups Promotes innovation Promotes job creation Supports the growth of enterprises and allows the future IPO in new sectors. To ensure compliance with the Sharia, Islamic crowdfunding must meet the following criteria: The platform should be managed by the Shariah Council. Investments should be socially responsible Startup activity should be Shariah compliant and should not generate revenue from sources that do not meet the Shariah rules. There should be clear limitations that in the future, the startup should exclude activities that are incompatible with Shariah. Shareholder structure and requirements for the protection of investors should be designed to comply with the principles of Sharia. 24 White Paper 1.0

25 The future of the digital economy and Islamic Finance As practice shows, crowdfunding corresponds to the norms of Islam and is also actively used in the practice of project financing, so there is no reason that crowdfunding based on blockchain technologies does not correspond to Islam. Considering the above, it possible to conclude that the idea of financing projects by means of crowdfunding in the cryptocurrency market conforms to the rules of Islamic finance. However, to select the correct transactions in the cryptocurrency market, it is necessary to be very careful in choosing the cryptocurrency, and the location of such transactions. Obviously, a huge number of cryptocurrencies do not comply with the rules of the Shariah and Muslims should beware of using them. At the same time, there are many projects that deserve attention and fully comply with the rules of Sharia. Muslims needs to understand that there are cryptocurrencies that are inherently haram by purpose of their creation, and also understand that the cryptocurrency market instability, because of its immaturity, is not a gharar, but only a stage in the formation of the market. Muslims needs a platform for dealing with the right cryptocurrencies, participate in the development of innovations, and encourage the creation of new unique projects and companies. ADAB Solutions was founded to create a platform for halal projects, to work in full compliance with the norms of Islam and Islamic finance. Our task is to help Muslims and the community of crypto-investors to differentiate the Shariah compliant products on the cryptocurrency market from the others. ADAB Solutions will generally benefit the market, since halal projects in their essence have utility and value, and will contribute to the development of useful ideas and a decrease in the number of haram projects in the market. White Paper

26 The future of the digital economy and Islamic Finance Problems of the Muslim Community 1. Absence of a crypto exchange, functioning in accordance with the norms of the Sharia. The absence of a cryptocurrency platform, guaranteed to work in accordance with the norms of the Sharia, keeps a significant number of Muslim investors from entering the cryptocurrency markets. 2. The lack of a unified position of the Muslim community on cryptocurrencies. In fact, this problem is the lack of systematic study of the cryptocurrency market and its key elements based on Shariah norms. Creation of the ADAB Solutions' crypto-exchange platform, the First Islamic Crypto Exchange, and the formation of the Islamic Finance Council will allow the formation of an interested community that systematically formalizes the work of cryptology on the basis of Shariah norms. 3. Uncertainty of Muslims regarding the admissibility of working with cryptocurrencies. Ethical uncertainty regarding the compliance of individual cryptocurrencies and the market as a whole with the norms of the Sharia leads to distancing, and as a consequence, the non-involvement of almost a quarter of the world's population in the technologically innovative financial sector. 4. Zakat is not paid from the turnover of existing crypto-exchange exchanges. One of the sacred pillars of Islam is paying zakat. Adab Solutions will deduct 5% of net quarterly revenue and 2.5% of annual net profit for charity. These deductions will form the basis for the charitable foundation Adab Charity Market Problems 1. The extremely low involvement of Muslims in the cryptocurrency market. The community of 1.8 billion people needs to create a cryptographic platform that functions in accordance with the principles of Islam. The creation of Adab Solutions and the First Islamic Crypto Exchange will create a huge new sector of the cryptocurrency market, and kick start the development of Islamic crypto-economics. 2. Lack of community trust in the key tools of crypto market. The cryptocurrency market needs self-regulation due to the formation of ethical standards of business management in the industry. The Adab Solutions' cryptocurrency platform, working in strict accordance with the principles of Islamic finance, guarantees security, honesty, transparency of business conduct, and complete absence of speculation in company activity. 26 White Paper 1.0

27 The future of the digital economy and Islamic Finance 3. Lack of new markets and investors. Dynamic development of cryptology depends on the constant attraction of new participants, and development in sectors of the economy. The ADAB Solutions project can become both a guide to the market for a Muslim audience and a platform for launching many halal projects The importance of the Adab Solutions project for participants and its uniqueness 1. The Adab Solutions project has no analogues in the world. Today, there is not a single cryptographic platform or a crypto exchange, which would guarantee activities based on Shariah law. Adab Solutions will be the first project that will perform cryptocurrency transactions in accordance with the principles of Islamic finance and on the basis of Shariah norms. 2. The Adab Solutions project is aimed at a huge audience of 1.8 billion potential Muslim users of the global cryptocurrency market. 3. Productivity of the project. The Adab Solutions project is designed in accordance with the highest security standards and has unique technical features. 4. The Adab Solutions project forms a system of values based on Shariah norms and principles of Islamic finance, which will become the basis for self-regulation of the cryptocurrency market and will increase the level of confidence in key cryptocurrency instruments. 5. Full transparency of the Adab Solutions project. Transparency of the project and safe jurisdictions will make it possible to buy and sell cryptocurrencies for fiat money on the exchange. 27 White Paper 1.0

28 Adab Solutions project Adab Solutions project 2.1 Objectives and mission of the project The ADAB Solutions project main goal is developing the FICE - First Islamic Crypto Exchange, based on Shariah norms. The purpose of the ADAB Solutions project is the creation of a crypto-exchange platform, a stock exchange, and services that comply with the norms of the Sharia and operate on the principles of Islam. The mission of the ADAB Solutions project is to create conditions and services based on the high moral and cultural values of Islam, and provide access to it to all users of crypto economics. The key task of ADAB Solutions is to create a structure that will establish new ethical standards for doing business in the industry. ADAB - standards of behavior prescribed by the norms of the Shariah, including good manners, standards of decency, courtesy, humanity. The name ADAB Solutions represents a big responsibility for the creators of the project. ADAB is a way of life in Islam, which the founders of the project consider not only natural in everyday life, but an obligatory foundation of business relations. ADAB Solutions is implementing the First Islamic Crypto Exchange (FICE) project. The Islamic Crypto Exchange is an alternative to investing in the cryptocurrency market, the main principles of which will be a ban on investments in gambling, usury, financial pyramids offering immoral services, as well as in companies engaged in the production of liquor and tobacco products. When there is suspicion of dishonesty in any company or its employees, or an indication of bearing excessive investment risk, investments in such companies will be deemed unacceptable, and they will not be admitted to listing on the exchange. White Paper

29 Adab Solutions project The above limitations must be considered not only for religious implications, exclusion of low-quality assets is a good basis for making reliable and safe investments. is a platform not only for Muslims and Islamic blockchain startups; it is an open marketplace for anyone who wants to build an honest technology business. Several jurisdictions and licenses are planned for FICE. The goals are to: minimize any risks, provide the ability to work with fiduciary money, including trading cryptocurrencies, enter and withdraw funds through banks. «Monotheism obligates to faith. Faith obliges to the existence of adherence to the canons. The canons oblige a person to be brought up. The one who is deprived of cultivation is far from the canons, faith and monotheism.» «Parenting is a strict adherence to that which embellishes deeds and actions.» 29 White Paper 1.0

30 Adab Solutions project Founder of ADAB Solutions Timur Turjan: «People should believe that cryptocurrencies are honest, reliable and safe. And in this we see a great opportunity for the market to use simple and obvious principles of honesty of Islam. Now there are no companies offering comprehensive solutions for Islamic crypto investment. We intend to solve this problem. Our clients and investors using our services will be sure that their actions are fully consistent with the principles of Islam, which will be confirmed not only by the opinion of our advisory council, but also by the opinion of experts and the general opinion of the community.» 2.2 Principles and values of the project The principles and values of the project coincide with the principles on which Islamic finance is based and are in turn based on the norms of the Shariah. Basic principles of the ADAB Solutions project: ADAB Solutions is guided in its activities by the values of Islam and the norms of the Shariah. ADAB Solutions guarantees that the FICE (First Islamic Crypto Exchange) exchange will have a ban on: a. credit transactions using interest, b. interest-bearing transactions, c. a gain on debt (riba- nasiya), and d. a gain on exchange (riba-fadl). e. ADAB Solutions guarantees that the FICE will have a ban on margin transactions with significant uncertainty (gharar). ADAB Solutions guarantees that the FICE will prohibit the use of the platform for financing certain sectors of the economy, including: gambling, production of pork, alcohol products and others (maysir), as determined by the Shariah Supervisory Board. White Paper

31 Adab Solutions project 4. ADAB Solutions guarantees the absence of excess Gharar in transactions (al-gharar al-kasir). Gharar (or speculative, excess risk) is not acceptable according to Sharia law. All types of transactions that will be technically possible on the exchange will be checked for a Gharar by the Shariah Advisory Board. At the FICE, under no circumstances will transactions be conducted to manipulate the market. This ensures compliance with the condition of sharing the risk of profit and loss between the parties to the transaction, in the case of operations involving such risks. The concept of Islamic finance is based on honesty, reliability and transparency based on the culture, ethics and principles of the Sharia. The ADAB Solutions project will demonstrate how the principles of Islam and Islamic finance will be implemented in a crypto currency project. 31 White Paper 1.0

32 Adab Solutions project 2.3 Solving key problems ADAB Solutions will solve the key problems that exist in Islamic crypto-economics and significantly inhibit its development ADAB Solutions will solve the problem of halal cryptocurrency transactions ADAB Solutions will create the FICE - First Islamic Crypto Exchange and guarantees to Muslims that it acts in accordance with the principles on which Islamic finance and the values of Islam are based. Muslims will receive an instrument that will allow Islamic finance and the Islamic economic system to use technologies that will determine the future of world finance ADAB Solutions will solve the problem of excessive risks in cryptocurrency systems Working on the principles of Islamic finance and following the norms of Sharia, ADAB Solutions will solve the problem of excessive risks in cryptocurrency systems by excluding the speculative component from the work of the exchange. This will allow us to stabilize the crypto-exchange platform, increase its reliability and protect FICE users from excessive risks, the adoption of which is directly prohibited by the Sharia in the course of transactions ADAB Solutions will solve the problem of developing Islamic crypto-exchange infrastructure Creation of a crypto-exchange platform ADAB Solutions and the First Islamic Crypto Exchange will lay the foundation for the development of a crypto-economic infrastructure. The creation of such an infrastructure will allow Muslims to gain access to innovative economic instruments. Currently there is no Islamic currency exchange. Therefore, there is no party guaranteeing its participants that there are no coins and projects in the listing that do not conform to the norms of the Sharia. After all, many cryptocurrencies are a haraam for Islam. We will create he world's first crypto exchange, which complies with Sharia law. First Islamic Crypto Exchange will become a universal solution for the involvement of Muslims and users of Islamic finance in the cryptocurrency market. The exchange will function according to the principles of Islam, but it is absolutely open to all users, of course, regardless of religion. White Paper

33 Adab Solutions project The lack of a single news portal, where investors can get information about both individual crypto currencies, and about blockchain projects that meet the norms of Islam, is also one of the problems that we intend to solve. ADABCRYPTO portal will be created as part of the project marketing strategy. On it will be published official fatwas, regulatory documents, and any news from the world of cryptocurrencies. It will also provide analytics and expert opinions, including a number of questions concerning the attitude of Islam to the industry as a whole, and to individual projects. Many Muslims are not informed or are mistaken about the compliance of crypto currency with Sharia law. Therefore, they avoid investing in any cryptocurrency assets. One of the most important features of our project is the management of the company in accordance with the Islamic management model, which supplements the generally accepted standards of business management. But the most important difference is that in our company one of the most important management bodies and decision-making centers will be replaced by the Shariah Advisory Board. All this will contribute to the fact that our company will provide high-quality information to the Muslim community about the cryptocurrency market, will carry out an explanatory mission, and facilitate the involvement of the Muslim community in the cryptocurrency market. Understanding this problem encourages us to create not only an exchange, but also a forum and a portal offering a comprehensive solution. Most crypto currency exchanges and news publications are published in English, Chinese, Russian, Korean and Japanese. Millions of investors, even if they understand spoken English, are forced to spend a lot of time to understand specific terms. Our stock exchange and other services will be multilingual. They will be available in English, Arabic, Indonesian, Malaysian, Russian, and also in Chinese. In the future, additional languages will be added in accordance with the geography of our users. 33 White Paper 1.0

34 Ensuring the compliance of the principles of Islamic finance Ensuring the compliance of the principles of Islamic finance 3.1 Islamic governance model ADAB Solutions integrates the Islamic management model into the management and business risk management system as an integral part of the company's management system. The Islamic governance model ADAB Solutions intends to follow will be based on the following approaches: Supervision of the management of ADAB Solutions on the compliance of activities with Islamic principles; The responsibility of ADAB Solutions for compliance with Islamic principles; The Shariah Advisory Board, which will oversee the compliance of ADAB Solutions practice with the norms and principles of Islamic law; 4. Implementation of internal Shariah supervision (Shariah Review); The work of the internal research and development department (Shariah Research); Perform regular audits of ADAB Solutions (Shariah Audit); 7. Managing the risk of non-compliance with Islamic principles; White Paper

35 Ensuring the compliance of the principles of Islamic finance 8. Development and publication of reports on the activities of ADAB Solutions, key provisions and expert opinions (resolutions). These requirements are consistent with the Islamic Corporate Governance System developed on the basis of the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) [16] and the Islamic Financial Services Board (IFSB), which ensures that ADAB Solutions will be managed in accordance with Islamic norms. 3.2 Council on Islamic Finance An important condition for the functioning of the Islamic Financial Institute is its compliance with the principles of Islamic finance. ADAB Solutions will create a Shariah Advisory Board (Council for the Observance of the Principles of Islamic Finance). The Shariah Advisory Board is a department consisting of experts in the field of investment, technology, and Islamic finance, which, in accordance with the Regulation on the Islamic Finance Council, ensures ADAB Solutions compliance with the norms of Islam in the implementation of FICE activities, listing of publicly offered crypto assets, and the development and approval of the standards and regulations governing the activities of the exchange. At the same time, the Islamic Finance Council is an independent body that monitors the principles of Islamic finance. The Shariah Advisory Board will make important decisions on admission to trading of a particular crypto currency. In addition to the standardized procedures for verifying compliance with Sharia law, the Council makes a final decision, the observance of which is mandatory for execution by the company's management and all its structures. Members of the Council are authoritative experts in the field of Islamic law and Islamic finance, experts in the field of Islamic banking and the cryptocurrency market. The minimum composition of the Council is at least 3 permanent members and at least 2 advisors. 35 White Paper 1.0

36 Ensuring the compliance of the principles of Islamic finance Council members will meet the following criteria: 1. To be a Muslim. A non-muslim cannot be a member of the council, even if he has the necessary knowledge in the sphere of Sharia and Islamic finance. 2. Have an economic or legal education. To solve financial problems and problems related to ADAB Solutions a religious education only is insufficient. A candidate for the Shariah Council will need an economic or legal degree. 3. To know the Arabic language. Arabic language proficiency will be necessary to interpret the provisions on the Islamic principles of financial relations contained in the Quran, the Sunnah and the writings of Muslim scholars. 4. Have experience in the field of Islamic finance. The management of ADAB Solutions will pay great attention to the experience of the candidates. White Paper

37 Ensuring the compliance of the principles of Islamic finance 5. Have an unblemished business reputation. An impeccable business reputation is essential not only for the management of ADAB Solutions and members of the Board, but also for all its employees. One of the options for strengthening the future responsibility of ADAB Solutions will be the formation of a two-level system of Shariah oversight. External and internal oversight will be implemented. Internal Shariah supervision will be implemented by the Islamic Finance Council, which will be formed within ADAB Solutions. External Shariah supervision will be carried out by representatives of an independent organizations authorized to carry out such questions. The tasks of external Shariah supervision will include checking the correctness of decisions made by the internal Shariah Council of ADAB Solutions. 3.3 Charitable Foundation ADAB Charity One of the sacred pillars of Islam is paying zakat. Zakat is called upon to establish societal principles of justice, mercy and honesty. According to the Shari'ah, its payment means that the incomes received and the acquired wealth are not sinful. Adab Solutions undertakes to deduct 5% of its net income for each quarter and 2.5% of annual net profit for charitable purposes. These deductions will form the basis for the charitable foundation Adab Charity. For all those who want to participate in charity, Adab Solutions will provide an opportunity to show virtue, make donations to support specific people who are acutely in need of it. Benefactors will be available information about what assistance was provided, to whom and in what size. A large amount of money will be earned in the crypto currency market, and Adab Solutions assumes that when working in cyberspace, in the sphere of high technologies, one should not forget about the need to help others who are in a difficult situation. 37 White Paper 1.0

38 Ensuring the compliance of the principles of Islamic finance Maintaining the integrity of society, helping and supporting individuals is the mission of the ADAB Foundation. The main task of the ADAB charitable foundation will be to support orphans, an educational mission, search for talented children and help them to obtain a quality education in the field of IT. ADAB Charity will cooperate with charitable foundations, and will provide all possible assistance, wherever it is needed. 3.4 Jurisdiction of the project Jurisdiction of the project ADAB Solutions is in UAE, Raz Al Khaimah. The choice is made as a result of an analysis of the key advantages of jurisdiction: A good investment climate for crypto projects, availability of banking services and favorable cryptocurrency regulation. The UAE is the most promising in terms of image, reliability and transparency of the company. The country is one of the world's biggest financial centers and centers of Islamic finance In the jurisdiction, relatively low costs for support personnel and transaction costs. The UAE has an excellent legal and regulatory framework, excellent opportunities for a company specializing in servicing clients on the principles of Islamic law. White Paper

39 lstamic crypt exchange (First lstamic Crypto Exchange) lstamic crypt exchange (First lstamic Crypto Exchange) Technical principles of the exchange FICE creates а technological service that will provide traders and investors with the optimal set of tools. The technical principles of FICE сап Ье formulated as follows: lnnovative and fast Matching Engine FICE The FICE platform will Ье one of the fastest crypto-instruments due to its аыility to process a multiple applications per second. Thus, users of FICE will Ье guaranteed that their applications will never Ье suspended due to congestion of the platform Continuous development of FICE functionality А. FICE will implement key functions of crypto-exchange В. The user's crypto. С. Spot trade. D. TechnicaL Analysis Tools Е. Unlimited withdrawal of funds. F. Trade in crypto-assets for fiat money White Paperl.O

40 Islamic crypt exchange (First Islamic Crypto Exchange) Support for trading pairs in key cryptocurrencies FICE will consistently expand the number of traded currency pairs. FICE will only list those coins that do not cause doubts in reliability, have a wide user base and high liquidity. An additional requirement will be the approval of the listing by the Shariah Advisory Board. FICE will support trading pairs in the following cryptocurrencies: - BTC - ETH - CRYPTO CURRENCY IN ACCORDANCE WITH THE DECISION OF THE SHARIAH ADVISORY BOARD Cross-platform trading clients and device support FICE will provide access to cross-platform trading clients: A. Browser client for Internet trading; B. Android user account; C. ios User Client; D. Mobile HTML5 Client Multilingual technical support FICE will support Arabic, English, Russian, Chinese, Malay, Indonesian languages on all user interfaces. The Alpha release of FICE is planned in English and Arabic. Additional languages will be added sequentially Trader rating Each trader trading on the FICE exchange will have its own rating, which consists of sub-ratings. The rating works using the blockchain. Accordingly, the rating cannot be falsified, corrected, or otherwise influenced by it. Investor who does not want to trade by himself can choose in the ratings section traders with good statistics. He can select a specific trader and view in more details his rating and sub-ratings. Then select the option to connect the Analytics (TSS - Trading signal system). And the trades of this trader will be automatically copied to the account of the Investor. For this service Investor pays money for a subscription. By default, only 20% of client s funds will be involved in trading using copying trader s trade deals. Investor can increase the percentage of his account traded on the signals of a particular trader to 100% or reduce it to 10%, thus copying transactions can be carried out from 1 to 5 traders at the same time. This option allows you to evenly distribute the risks of the investor. White Paper

41 The rating is based on taking into account the efficiency of trading results of each trader and depends on certain factors: - the duration of trade (ranks depending on the period for the week, month, year and for the entire period of trade). The rank can be made public only after a certain time, at least 3 months of trading - only net income is taken into account (the calculation is based on the current balance of the trader, taking into account only recorded trading operations) - account size (a certain gradation of accounts according to their size will be created). Why is it important? - it is quite easy to increase a small deposit by constantly risking and trading non-systemically. On small accounts, generally, beginners trade. Big money - more responsibility, big account and long-term positive trading are the key to investor confidence. - account currency. Also, one of the components of the overall rating should be the sub-rating, the value of which is determined by the trading activity of the trader and the number of his subscribers. It is necessary so that with the growth of the value of this sub-rating, the commission for the trader would decrease and at some point it would become minimal for him. The commission may become zero for the trader and, moreover, he may receive a commission from the trade of his subscribers. The more subscribers and more than the number of trade operations, the higher the value of this sub-ratings and more receives a trader. Depending on the value of this sub-rating, a trader can receive from 10% to 25% of the commissions paid by its subscribers. All these factors and technical innovations will allow FICE to attract a large number of professional and experienced traders from the first day of the launch of the exchange. First Islamic Crypto Exchange Generation Islamic crypt exchange (First Islamic Crypto Exchange) Source Commission for currency exchange Commission for withdrawal of funds The listing fee Other commissions Description The commission for currency exchange will be charged at a fixed rate of 0.05% to 0.2% per transaction Commission for withdrawal is not charged, with the exception of that held by the bank in the derivation of the funds First Islamic Crypto Exchange will make a decision on listing tokens based on their compliance with the principles of the exchange and charge a listing fee depending on the current trading volume There may be commissions for services rendered by third parties in favor of First Islamic Crypto Exchange customers According to the Roadmap and the current rate of development, the FICE will enter the top ten world exchanges within 12 months. 41 White Paper 1.0

42 Islamic crypt exchange (First Islamic Crypto Exchange) White Paper

43 Islamic crypt exchange (First Islamic Crypto Exchange) The forecast commission will be 0.2%. The size of the commission corresponds to the average market values. Other incomes - exchange fees for withdrawal of fiat funds in the amount of 1%, as well as fees for listings and launch of projects on the ADAB Project platform. The turnover of the exchange depends on many factors, both internal and external. Graph of growth in trading volumes and total income of the FICE exchange Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct-2024 Volume of trade, thous $ / month Total revenue of FICE, thous $ Thus, the First Islamic Crypto Exchange is expected to reach a daily trading volume of about $ 146 million and a monthly turnover of $ 4.4 billion during the first year of the exchange's operation. 43 White Paper 1.0

44 Islamic crypt exchange (First Islamic Crypto Exchange) Thus, as follows from the table of the forecast for achieving the turnover of the First Islamic Crypto Exchange and the total income of the exchange, ADAB Solutions' crypto-exchange platform is capable of generating a significant income, however, in the first year of implementation costs and expenses can significantly exceed profits. The difference between the costs and the profit generated by the ADAB Solutions crypto-exchange platform is planned to be covered from the funds raised during the ICO. 4.3 Security of the Exchange FICE security will be provided both by the best developments in the field of cybersecurity and by the high level of business transparency. This will be ensured by the transparency of the key processes of ADAB, and also by an independent governing body - the Shariah Advisory Board. FICE organizes a secure development life cycle (SDL), which will adhere to all industry standards. FICE implements threat modeling and STRIDE analysis, static code analysis (SAST), dynamic code analysis (DAST), and hacking testing. FICE will use the encryption standards recommended by NIST (AES-256, SHA256 / SHA3) and will not use proprietary encryption schemes. All user data, including internal traffic, will be encrypted. FICE guarantees that: A. All sensitive data will be encrypted using the AES-256 encryption protocol; B. During the transfer of data will use the protocols TLS 1.2; C. The FICE site will use SSL certificates of high reliability (EV SSL); D. Passwords and keys will be stored using one-way hashes (SHA3); E. FICE will support internal operational security protocols approved by ADAB; F. FICE organizes regular audit of certificates and safety protocols. White Paper

and to provide access to ADAB Solutions products to a wide")

45 ICO and token ADAB ICO and token ADAB 5.1 ADAB token First Islamic Crypto Exchange implements the possibility of users purchasing ADAB tokens within the framework of ICO. The purpose of the ICO is to raise funds for the development and scaling of the Islamic crypto-exchange (First Islamic Crypto Exchange) and to provide access to ADAB Solutions products to a wide range of users. ADAB's Islamic ADAB tokens are based on the ERC20 standard and are subject to automatic execution upon the occurrence of pre-specified conditions. ADAB's tokens are the property of their owners and provide full unconditional access to the products of the Islamic First Islamic Crypto Exchange. ADAB token holders cannot influence the team of the First Islamic Crypto Exchange on decision-making and business related activities. ADAB's tokens are not securities, shares or their equivalent, and do not give the right to ownership of First Islamic Crypto Exchange. The ADAB tokens will be distributed in accordance with the rules and conditions in proportion to the amount transferred by users during the ICO. The ADAB token will be accepted as a means of payment for the products of the First Islamic Crypto Exchange and its partners. The ADAB token can be freely exchange for fiat money and other cryptocurrencies. Users will be able to buy and sell ADAB tokens, the ADAB token value will be determined on the basis of supply and demand on the First Islamic Crypto Exchange and later on the basis of open market, after listing the ADAB token on exchanges. 45 White Paper 1.0

46 ICO and token ADAB 5.2 Conditions for ICO ADAB tokens will be distributed in accordance with the rules and conditions in proportion to the amount transferred by the ADAB Solutions participants during the ICO. ADAB tokens can be used for payment of all ADAB Solutions services and, in addition, can be converted to ETH / BTC / USD on the open market. After the ICO, ADAB token will be listed on key exchanges, and after the launch of its own exchange, also on FICE. The first listing is expected within 30 days of the completion of the ICO. Terms of ICO The technical limit for the release of tokens The volume of sale of tokens for sale and as possible bonuses Soft Cap Hard cap The price of the token in USD Acceptable form of payment End date of Stage 1 - closed pre-sale Start date of Stage 2 - pre-sale End date of Stage 2 - pre-sale Start date of Stage 3 - crowd sale End date of Stage 3 - crowd sale Token issue date The launch of a smart contract Listing on Exchange The minimum volume of redemption of ADAB tokens $ 2,500,000 $ 18,700,000 $0.1 ETH, BTC before before not earlier then ADAB The maximum volume of redemption of ADAB tokens (excluding bonuses) ADAB White Paper

Bounty-company (1%) Reserve fund (18%) Advisors and experts")

47 ICO and token ADAB The price of the token and the number of tokens distributed do not mean that the company can collect more funds. Charges are terminated upon the achievement of the project s hard cap. The cost is determined on the basis of the maximum possible coefficients for increasing the transferred bonuses (1.85). 5.3 Distribution of tokens Reaching the ADAB token begins with the initial distribution of tokens during the ICO by the initial exchange rate of 0.1 USD. ADAB Solutions issues a maximum of 350,000,000 ADAB tokens at an initial cost of 0.01 USD per 1 ADAB token. Start cost of the ADAB token will be estimated at 0.1 USD. The only release of ADAB tokens will occur during the ICO and will become a preliminary sale of access to the use of ADAB Solutions services. Distribution of ADAB tokens Participants of pre-ico and ICO (70%) Founders and team (8%) Bounty-company (1%) Reserve fund (18%) Advisors and experts (3%) 70% - the total share of tokens distributed among the community during pre-ico and TGE; 1% - tokens allocated for marketing purposes and Bounty-company; 18% - - the creation of a reserve fund, stabilizing the work of ADAB Solutions and the cost of the token; 8% - team; 3% - advisers. 47 White Paper 1.0

48 ICO and token ADAB The tokens destined for the ADAB Solutions team will be frozen and will be unlocked: 25% immediately after the completion of the ICO, 25% after next 6 months, 50% after 12 months since completion of the ICO In case if an employee has got dismissed for any reason, the company has the right to return part of frozen tokens. From the 8% of tokens destined for a team, no more than 4% will be used for payments to the team members who participated in the ADAB Solutions ICO project. The remaining tokens will be distributed between current and future members of the team in recognition of achievements, implementation of individual and collective plans. Tokens do not belong to the founders of the project, they belong to the company. Tokens of the advisers will be frozen and will be unlocked: 25% immediately after the completion of the ICO, 25% after next 6 months, 50% after 12 months since completion of the ICO The tokens from bounty campaign will be frozen and will be unlocked: 25% immediately after the completion of the ICO, 25% after 3 months since the completion of the ICO, 25% after 6 months since completion of the ICO, 25% after 9 months since completion of the ICO Tokens of the advisors not paid to the advisers will be credited to the reserve fund. Subsequently, they can be paid to the advisers involved at the stage of the company's activities. Reserve fund tokens - are used to stabilize the work of the exchange, to test the platform, marketing activity to attract new users of the platform, and for other purposes aimed at the development of the platform Reserve fund tokens have no turnover limit. White Paper

49 ICO and token ADAB ADAB Solutions will focus on providing solutions, products and functions of the FICE exchange, which can be quickly and effectively implemented, increasing the relevance, speed and value of ADAB tokens. ADAB Solutions will ensure the availability of tokens owned by people who buy ADAB tokens no later than May 25, 2019, provided they provide the necessary information. ADAB token distribution can occur before June 10, but ADAB tokens will be inactive, they cannot be used and exchanged. The only release of ADAB tokens will occur during the ICO and will essentially be a preliminary sale of access to the use of ADAB Solutions services. Implementation of ADAB tokens occurs in 3 stages: Stage 1 - close pre-sale, Stage 2 - pre-sale, Stage 3 - crowd sale. 49 White Paper 1.0

50 ICO and token ADAB Additional bonuses for participants Bonuses for the participants of Stage 2 - pre-sale Dates before The rate of increase in the volume of transferred tokens Pre Sale 1,05 Minimum purchase amount 1000 ADAB Bonuses for the participantsof Stage 3 - crowd sale Dates The rate of increase in the volume of transferred tokens 1 The Company has the right to apply raising coefficients based on the results of negotiations, but not more than the maximum possible coefficients Tokens accrued as bonuses will be frozen and will be unlocked after 12 months since the completion of the ICO. Fees are recorded in US dollars 50 White Paper 1.0

In the case of incomplete sales of implemented tokens during the tokensale (sales less than 245 million")

51 ICO and token ADAB 70% of ADAB tokens will be implemented during the tokensale. Fundraising stops when the hard cap project is reached. The maximum possible number of tokens sold is 245,000,000 (including tokens accrued as bonuses) In the case of incomplete sales of implemented tokens during the tokensale (sales less than 245 million tokens) all unsold tokens will be transferred to the reserve fund. In the case of collecting of more than 18.7 million (sales of tokens with a lower bonus coefficient), additional funds will be directed to additional marketing goals and for attraction new users on exchange. 5.4 Forming the value of the token The internal economy of FICE is built on the deflation model of ADAB token and is calculated on the basis of the monetary equation that relates the quantitative volume of issued tokens and their price needed to service the planned transactions. This will ensure the forecasted rate of the token and stabilize the domestic economic processes of the platform. In developing the economy of thefice, ADAB Solutions took into account both key aspects of the monetary policy of regulators and other external factors that will affect the price of ADAB tokens.. Payment of commissions within the Islamic Currency Exchange FICE will be accepted only in ADAB tokens, which serve as a key to accessing the services of the platform. White Paper

52 ICO and token ADAB The purchase of ADAB tokens will be made automatically at exchange rate on the time of transaction in the amount sufficient to pay the commission fee. The growing demand for ADAB tokens with volume growth and the introduction of additional products will increase the cumulative volume of transactions within the First Islamic Crypto Exchange, which will also affect the price change of the ADAB token. Commissions used in ADAB tokens are the basis of FICE's revenue, which causes ADAB Solutions' interest in maintaining a stable exchange rate and liquidity of tokens. Therefore, to support the deflation of the token, 10% of revenue, but not more than 30% of net profit in ADAB tokens will be burned every month, not returning to circulation. This will help to systematically reduce the total number of tokens in circulation, which, combined with the increase in the volume of transactions, will lead to a predicted increase in the rate of the token. The burning of the tokens will be done until the 50% of the initial emission is paid off. The remaining tokens will remain in circulation to ensure the intra-exchange turnover. Period Volume of trades, thousand dollars per month The minimum price sufficient to service turnover,$ Forecasted value of the token, $ Q3, ,10 0,12 Q4, ,22 0,24 Q1, ,49 0,49 Q2, ,98 0,98 Q3, ,24 1,36 Q4, ,39 1,66 Q1, ,98 2,57 Q2, ,53 3,54 Q3, ,30 4,96 Q4, ,58 5,72 Q1, ,85 6,55 Q2, ,13 7,43 Q3, ,41 8,38 Q4, ,69 9,38 Q1, ,98 10,45 Q2, ,26 11,58 52 White Paper 1.0

53 ICO and token ADAB Schedule of growth of the value of the token 14,00 12,00 УAловите свое 10,00 8,00 6,00 4,00 2,00 0, The minimum price sufficient to turnover service Forecast price Schedule of growth of the value of the token. These calculations are based on the maximum possible release of ADAB tokens, the fewer tokens that are released, the greater the increase in value. After the completion of the ICO, the calculations will be updated. The project covers a huge audience, for the first time in the cryptocurrency market the broadest geographical, social, age, and gender coverage of the target audience. Being a participant in the creation of the world's first Islamic crypto exchange is a great opportunity to contribute not only in the development of the industry, but also in the creation of new moral values and benchmarks in the cryptocurrency market. White Paper

54 ICO and token ADAB 1. All unsold ADAB tokens will not be burned after the completion of ICO, they will be tranfered for the Reserve Fund. Capital of this Fund can be used: to stimulate traders (loyalty program, consisting in paying remuneration to traders, depending on trading activity), to attract traders to the exchange platform (certain payments to the traders who come to the FICE and fulfill certain conditions - the amount of the deposit, period of stay on the platform), on the development of partnerships, on other payments that stimulate FICE s development to increase the customer base. 2. ADAB tokens can be used as a payment instrument on the FICE. Using ADAB tokens as a commission fee gives an advantage in the form of a discount on commissions up to 20%. 3. Accepted methods of payment - USD, AED, BTC, ETH 54 White Paper 1.0

55 ICO and token ADAB Key factors on which the functioning of the ADAB token will be based: The token is the access key and the only way to pay for all ADAB Solutions products and services. The initially issued number of tokens is the maximum and the final, additional emission is not provided. 10% of revenue, but not more than 30% of net profit in ADAB tokens will be burned every month, without returning to circulation. This will lead to a smooth decrease in their number and a decrease in the total offer of tokens. Tokens will be burned until their total volume is 50% of the initial emission. The remaining tokens are needed, since they perform a billing and negotiating function on the ADAB Solutions platform, they pay for services and services. Since tokens perform a reverse and payment function on the ADAB Solutions platform, the need for them will grow with the increase in the volume of transactions. You can meet the growing demand by increasing the number of tokens or increasing the bid price. The number of tokens will not increase, it will decrease due to the fact that part of the tokens will be burned. The only way to meet the growing demand for a decreasing number of tokens is to increase the exchange rate of the token. 55 White Paper 1.0

56 ICO and token ADAB Advantages of the ADAB token: FICE is the first Islamic crypto exchange. Great potential for the development of the project and the growth of the client base. The project solves the global problem of Muslim involvement in the cryptocurrency market. The company will burn tokens every month, which will reduce their number with growing demand, this will in turn contribute to a stable growth of the token rate. The volume of commissions received can be easily traced, which will not allow manipulating the volume of funds allocated for the redemption of tokens. To be the first in the world to offer a quality solution for Muslims in the market of cryptocurrencies is the most important factor in the value of investments in ADAB. The significant potential of the demand for our services and their uniqueness is the basis for a fast-growing and profitable business. The idea of popularizing crypto-investments through qualitative services based on the principles of Islamic finance has not only a commercial but also a significant ideological context. This should favorably affect the growth of our project and its further development. White Paper