ISLAMIC SOCIAL FINANCE REPORT. 15 June

|

|

|

- Reynold Brown

- 6 years ago

- Views:

Transcription

1 ISLAMIC SOCIAL FINANCE REPORT 15 June

2 Islamic Social Finance (ISF) Report: Objectives Study on Zakah, Awqaf and Islamic Microfinance Sectors with the following key objectives: Estimate trends in flow of funds Undertake comparative analysis of enabling environment, e.g. regulations Document good practices of key players Contribute to policy dialogue for development of the ISF sector & facilitate reverse-linkage strategy of IDBG Islamic Research and Training Institute Member of the Islamic Development Bank Group

3 Islamic Social Finance (ISF) Report: Structure Region under Focus: key economic and poverty-related indicators, potential of Islamic social funds in meeting resource gaps for poverty alleviation Zakah Sector: Trends in zakah mobilization and distribution; comparison of enabling environment; good practices at micro and meso levels Awqaf Sector: Estimates of existing awqaf; comparison of enabling environment; good practices at micro and meso levels Islamic Microfinance Sector: Trends in Islamic microfinance development; comparison of enabling environment; good practices at micro and meso levels Islamic Research and Training Institute Member of the Islamic Development Bank Group

4 15 June

5 ISF: Region under Focus Muslim Population (2013/2014) Country Total population Muslim population % of Muslims in total population Kenya 44,354,000 3,104, Mauritius 1,257, , Nigeria 173,615,000 83,161, South Africa 52,981, , Sudan 37,964,000 27,106, Tanzania 44,928,923 13,433, Source:

6 Challenge of Poverty Alleviation country year Poverty headcount ratio at $1.25 a day (PPP) (% of population) Poverty headcount ratio at $2 a day (PPP) (% of population) Poverty headcount ratio at national poverty line (% of population) Kenya Nigeria South Africa NA Sudan Tanzania (2012)

7 Potential of ISF for Poverty Alleviation Country Resource Shortfall under USD 1.25 per annum as % of GDP Resource Shortfall under USD 2.0 per annum as % of GDP Z1 (% of GDP) Z2 (% of GDP) Kenya Mauritius NA NA Nigeria South Africa Sudan Tanzania Z3 (% of GDP)

8 Trends in Zakat Collection and Distribution

9 Sudan

10 Issues in Zakah Collection in Sudan General Lack of public awareness of the mandatory nature as well as the rules of zakat Low levels of awareness among relevant stage agencies as regards their legal obligation to support the Diwan in its collection efforts Positives Growth in crop s share in areas of relative stability Growing accumulated experience of Diwan officials Islamic Research and Training Institute Member of the Islamic Development Bank Group

11 Issues in Zakah Collection in Sudan Crops: High variability attributable to Natural and climatic factors; Security conditions faced by some areas; Problems unique to large agricultural projects; Decline in the contribution of small irrigated schemes due to the high costs of agricultural production Overall, monitoring costs are quite high Large tracts of land are difficult to reach; Leakages are hard to control in view of multiple entry points to major cities; Many of the products are stored at the sites of production making it difficult to monitor Islamic Research and Training Institute Member of the Islamic Development Bank Group

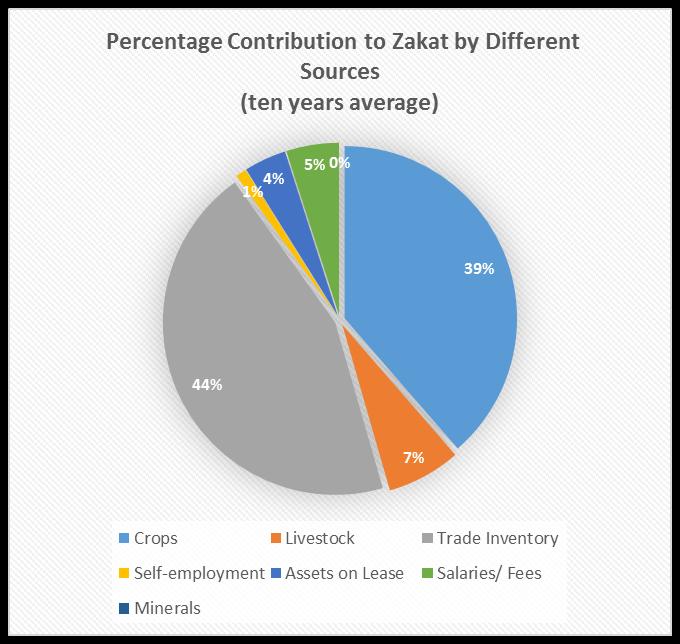

12 Issues in Zakah Collection in Sudan Livestock: Contributes significantly more than crops - to the GDP Dominant form of zakatable wealth in regions, such as, Darfur and Kordofan, but contributes a meagre 7 percent to total zakat Widespread instability in the regions with large herds of livestock Opaqueness of national boundaries across which the herds move in search of pastures Owners of livestock are a difficult people of deal with and monitor; keep changing their locations Mining: Large chunk of gold held by families Private and illegal mining Islamic Research and Training Institute Member of the Islamic Development Bank Group

13 Issues in Zakah Collection in Sudan Trade Inventory & Business: Lack of coordination between state zakat body and the banking system; zakat due on bank deposits of 23,416 million SDG was million in 2013, a sum equivalent to 115.8% of the total collection under trade and business Lack of coordination between the Registrar of Companies and the Diwan Zakat; the number companies that pay zakat is less than one-tenth of the over forty thousand registered companies Absence of any linkage between customs clearance procedures and zakat payment Little option but to accept the zakat allocated by the Auditor General in resepect of investment by government bodies and companies Understaffed Diwan, though it performs a function comparable to IRA Islamic Research and Training Institute Member of the Islamic Development Bank Group

14 Issues in Zakah Collection in Sudan Overall: Weak implementation of Article 49 that requires presentation of zakat settlement certificate before certain transactions can be completed, in view of continued resistance on the grounds of public grievance e.g. payments from the government bodies; registration of companies, co-ownership, business names and trademarks register; registration, or renewal of registration in the register for importers and exporters; registration of ownership of real estates; participation in government auctions; obtaining licenses, renewal and transfer of ownership of commercial and rental vehicles, harvesters and tractors; obtaining and renewal of trading licenses; seeking approval of erecting multistory buildings etc. Islamic Research and Training Institute Member of the Islamic Development Bank Group

15 State-wise Zakat Collection in Nigeria Year Total Zakat Collection ZSF(Lagos) Bauchi Zamfara 92, , , , , Kazaure Dutse 149, , , , , Kebbi Kano Sokoto Niger Total

16 South Africa National Zakat Fund (SANZAF) Year Zakat Non-Zakat Total Zakat

17 Mozambique There seems to be a total lack of awareness among the public about zakat. The voluntary actions by the Muslim community was in response to severe floods a couple of years back. Charity in general, is a tax deductible expense and total collection of charity funds by the community was in the range of USD300,000 over last 3 years.

18 Tanzania There are a few NGOs who collect and distribute zakat, the largest being an association of Yemeni brothers and sisters, who are among the richest in the country. There is no national body for management of zakat and zakat is not mandatory. Therefore, there is hardly any accurate information about collections.

19 Mauritius This is a country with a sizable number of well-to-do Muslims and several Muslim NGOs. However, zakat collection and distribution is undertaken privately and voluntarily.

20 Kenya Unfortunately, there is no organized effort for collection and distribution of zakat here in spite of the huge Muslim population. Notwithstanding the presence of many rich Muslims in Kenya, they seem to pay on their own.

21 Zakat Distribution

22 Average Zakah Distribution in Sudan ( ).docx Fuqara and Masakin Gharimeen Ibn Sabeel Muallaf Fi Sabilillah Amileen Alaiha Administrative Expenses Islamic Research and Training Institute Member of the Islamic Development Bank Group

23 Issues in Zakah Distribution in Sudan Poverty Alleviation with Zakah An allocation ratio of over two-third to the poor and the needy Within this overall category, further prioritization in favor of orphans, widows, sick and infirm, elderly and university students who come from poor families. Support and assistance in the form of projects (project health insurance, project uniforms, project to finance university students, project to sponsor orphans etc.). Focus on productive projects that benefit from a specified allocation. Support to States that are suffering from problems of displacement, war and contribute to the stability and resettlement of returnees. Implementation of collective projects and service projects that address issues of mass poverty (water, health, education).

24 NIGERIA Zakat Allocation among Beneficiaries in Sokoto Health Mentally ill Person Food Assistance Shelter & Rehabilitation Human Resources Development Orphans

25 South Africa Distribution of Zakat SANZAF is committed to utilizing the bulk of its resources directly on and for the benefit of the poor and needy. Desires to transform its beneficiaries from recipients (Mustahiq) to payers (Muzakki) of zakah and was borne out of a realisation that handouts (welfare) were not sustainable in the long run It is now committed to allocate at least 60 percent of its collections towards developmental initiatives. spends 25 percent of its income for education alone.

26 Enabling Environment for Zakah Sudan: Zakat Act 2001 Nigeria: section 4, sub section 7 of the 1999 Federal Constitution, gives rooms for introduction of Shariah in any state that wishes to do so. The list of the laws covered in this section include the following: Bauchi State Zakat and Endowment Fund Collection, Administration and Distribution Law, 2003 Zamfara State Zakat (Collection And Distribution) and Endowment Board Law, 2000, 2003 Niger State Zakkat (Collection and Distribution) and Endowment Board Law, 2001 Zakat Collection and Distribution Committee Law 2000, Jigawa State Kano State Zakat and Hubusi Commission Law 2003 Katsina State Sharia Commission Law, 2000 Borno State Zakat and Endowment Board Law, 2001 Yobe State Religious Affairs Board 2001 Kebbi State Zakat and Sadaqat (Collection and Distribution) Board Law, 2000 Islamic Research and Training Institute Member of the Islamic Development Bank Group

27 South Africa S.Africa has a law for non-profit-organizations that is relevant for its organizations engaged in mobilization of zakat and awqaf. Except the above none of the countries from sub-saharan Africa covered in this report have dedicated laws for zakat management

28 Zakat payment : Compulsory or Voluntary Sudan: Compulsory. Sudanese law does not impose any physical penalty on defaulters, but provides for forced recovery of due and unpaid zakat.(execution through competent court). Tax Incentives: When the income tax of any person is assessed, the zakat paid by him shall be deducted from his property assessed for income tax, provided that, zakat deduction shall not be duplicated.

29 Zakat payment : Compulsory or Voluntry Nigeria: Provinces like Bauchi, Zamfara, Niger and Jigawa States have made zakat payment compulsory. Punishment on non-opayment Vary from state to state (fine half of payment of zakat to full, three to 6 months imprisenment etc.). No tax exemption. Kano, Katsina, Borno, Yobe and Kebbi states make zakat payment a voluntary act. Zakat payment is also voluntary in other countries covered in this report, e.g. South Africa, Kenya, Tanzania and Mauritius.

30 Institutional Structure for Zakat Management Chart : Institutional Structure for Zakat in Sudan

31 Nigeria: Dutse Institutional Structure for Zakah Management Emirates Main Committee General Policy on Distribution Local Govt. Committees Assessment and Collection Policy District Committees Coordinate Assessment and Collection Ward Level Committees Storage & Final Distribution to the Poor and Needy Village Level Committees Assessment & Collection Supervision Census & Data

32 Major findings in relation to the zakat sector. Differences in geo-politic realities affect zakat management. There is thus, great diversity in the zakat management practices. With the exception of South Africa, in all countries a major part of zakat is in the nature of in-kind zakat in the form of crops and livestock. Zakat collected as cash is very insignificant. Therefore, holding of zakat funds or investment of zakat funds is a non-issue. Collection of in-kind zakat from the actual locations, e.g. farms, that are stretched far and wide entails huge collection costs. Therefore, a more liberal view is called for in relation to the cap on operational costs that is traditionally placed on one-eights of zakat funds collected. Further, once zakat is collected, their transportation and storage of in-kind zakat involves substantial costs, which justifies the strategy of on-the-spot distribution. While in Sudan and four states in Nigeria, zakat is mandatory, the same is voluntary in other states of Nigeria as well as in the other countries under focus. In Sudan zakat has been steadily increasing at an annual average growth rate of 19 percent. But In some states of Nigeria did not perform well. A vibrant network of organizations at different levels is important. In Lagos (Southern Nigeria) for instance, where state plays no role and zakat management is in private hands, the handful of voluntary zakat organizations seem to have performed well. Similarly, in South Africa, the voluntary zakat organizations have reported excellent performance. Irrespective of whether zakat is compulsory or voluntary, a policy of decentralization seems to have paid off.

33 Major findings in relation to the zakat sector. The case for having standardized and globally acceptable definitions of zakatable assets and methods of estimating zakah liability does not appear to be a strong one. Since Islamic societies are typically characterized by multitude of madhabs and schools of thought, the zakat laws must retain enough flexibility to accommodate alternative views. The diversity in legal opinions should be respected. However, in societies like Sudan with greater homogeneity in Shariah-legal positions, and where zakat is compulsory, the inclusion of definitions and methods seems to have imparted greater stability and added to enforceability. Where zakat is voluntary, it is more practicable to ensure that zakat estimation is an outcome of consultative processes between the muzakki and the zakah collecting institutions. The zakat sectors in Sudan and South Africa provide supporting evidence that the success or failure of an institution as zakah collector and distributor is not so much dependent on whether it is in government or private hands, but on the credibility and trust it enjoys among the muzakki population, which in turn are a function of the integrity, transparency and good governance reflected in its practices and as perceived by the stakeholders.

34 Major findings in relation to the zakat sector. Where zakat is subject of a state, zakat may be seen as a component of aggregate resources available to the state and it may be seen as a perfect substitute of the direct taxes to the state and may be allowed as deductions to tax payable. However, there must be absolute clarity on the issue as well coordination between zakat and inland revenue bodies. The absence of clarity seems to have affected zakat collection in Sudan adversely in the initial stages of operation of the Diwan, but sorted out later with tax incentive being made available only on zakat paid on salaries. In the Nigerian states, on the other hands, the difficulty in coordination between the agencies seems to have resulted in withdrawal of the incentive itself creating further confusion. Zakat manaement in Sub-Saharan Africa in general seems to have suffered a great deal due to absence of meso-level organizations, e.g. networks, training and education providers, consultancy and standard-setting bodies and advocacy organizations. As a result, public awareness about zakat obligations is extremely low in many part of the region. Data is extremely scarce. Some specific policy recommendations may be made in the context of in-kind zakat like crops and livestocks. Due to the vast expanse of agricultural areas and given the hugeness of the monitoring task, Zakat mobilization should actively involve local committees as a way to build social capital and enhance community solidarity. Local participation should be sought in the collection of zakat on agricultural products of smallholdings, and inventorize merchandize and leased property in the locality. Zakat should be distributed in the neighborhood in order to encourage them to contribute to community solidarity. A large proportion of cattle collected as zakat should be distributed at the collection area itself to save on costs of transportation and storage.

35 Key Findings on Awqaf Sector Enabling Environment Examples of Good Practices Islamic Research and Training Institute Member of the Islamic Development Bank Group

36 Enabling Environment for Awqaf Sector Sudan: the waqf laws has undergone continuous reforms. Now a new law called "the Diwan of the National Islamic Endowments Act of 2008". Nigeria: The Nigerian states have made recent legislations dedicated to waqf which are yet to show their impact. The list of the laws are: 1. Bauchi State Zakat and Endowment Fund Collection, Administration and Distribution Law, Zamfara State Zakat (Collection And Distribution) and Endowment Board Law, 2000, 2003.docx 3. Niger State Zakkat (Collection and Distribution) and Endowment Board Law, Zakat Collection and Distribution Committee Law 2000, Jigawa State 5. Kano State Zakat and Hubusi Commission Law Katsina State Sharia Commission Law, Borno State Zakat and Endowment Board Law, Yobe State Religious Affairs Board Kebbi State Zakat and Sadaqat (Collection and Distribution) Board Law, 2000 Mauritius and Zanzibar in Tanzania have well-established waqf laws. South Africa offers a good example of waqf development in the private and voluntary domain. Islamic Research and Training Institute Member of the Islamic Development Bank Group

37 Key Policy Findings Definition Waqf law should provide a comprehensive definition of waqf that includes both permanent and temporary waqf. It must explicitly cover various types of waqf: family and social waqf, direct and investment waqf, cash waqf, corporate waqf. Except Sudan and Nigeria, legal frameworks in most countries do not explicitly deal with cash and corporate waqf. Laws in Sudan and Mauritius include provisions regarding family waqf.

38 Creation of New Waqf: Remove obstacles Legal requirements that make the creation of new waqf more difficult, e.g. approval of the head of the state, are both unnecessary and undesirable. A simple process of registration with the regulatory body is both desirable and adequate. Creation ofwaqf in countries, e.g. Zanzibar (Establishment of Masjids) require prior permission.

39 Creation of New Waqf: Encourage Citizens The legal framework should actually encourage creation of new waqf by minimizing financial and non-financial costs of waqf creation and management. A major objective of the Diwan in Sudan isto carry out training and capacity building and institutional development in the field of waqf and encourage citizens to do waqf. In Zamfara state in Nigeria, the government agencies and contractors are required to endow a certain percentage of their total revenues as waqf thereby, ensuring the continuous enhancement of waqf corpus. In Zanzibar however, there are checks on creation of new waqf. Section 17(3) asserts that the creation of any private waqf after commencement of the Act shall be invalid unless registered by the Commission.

40 Creation of New Waqf: Who Can Do Waqf Most laws restrict making a waqf to Muslim individuals Kenyan law even restricts it further by using narratives, e.g. an Arab, a member of the Twelve Tribes, a Baluchi, a Somali, a Comoro Islander, a Malagasy or a native of Africa of the Muslim faith Law should permit non-muslims as long as the purpose of waqf is religious or charitable

41 Creation of New Waqf: What may be Endowed The legal framework should not restrict the definition of the endowed asset to immovable tangible assets, such as, real estate, but should also explicitly recognize movable, financial and intangible assets, e.g. cash, stocks, bonds and financial securities, transportation vehicles, rights on land and building, rights of leasing, rights of intellectual property. Nigerian law permits waqf of all lawful items permitted by Shariah. In contrast, in Mauritius, the law requires that the subject of waqf may consist of any property other than things which are consumed by use.

42 Creation of New Waqf: Revive Family Waqf The institution of family waqf must be revived. Sudan and Mauritius provide some excellent examples of family awqaf. The law in Mauritius has a few interesting features: the possibility of restricting the benefits to one or two generations, the need for concurrence of wife before a husband may make a waqf, how waqf benefits will be apportioned between children and descendants and other possible beneficiaries across generations and between males and females, and finally, the conditions under which the benefits will lapse.

43 Waqf Management: Recovery of Lost Waqf Legal frameworks must clearly articulate the permanent nature of waqf arising from the principle of once a waqf, always a waqf. In case old laws fail to ensure protection, they must be replaced with new provisions that enable recovery of lost waqf assets. Sudanese law empowers the Diwan to recover all the endowed money which is possessed by other individuals, institutions, companies, or governmental authorities or to receive a just and equitable compensation from them; that excludes endowments from application of any superseding law and that applies the provisions of the evacuation of public buildings Act to endowments. Zanzibar law provides recovery of all waqf that had remained outside the purview of the commission.

44 Waqf management: Preservation vs. Development The regulatory framework must seek to strike a balance between concerns about preservation and development. Sudanese law seeks to strike a balance between preservation and development aspects by requiring the Diwan to undertake the maintenance and improvement of endowed funds and evaluation, construction and re-construction, and investment offunds in all legitimate investments. In Zamfara and Bauchi states the law briefly touches upon development aspects of waqf and mentions in sections 5 and 3 respectively that the Board/Commission must invest endowment funds in ways that will meet the objectives and purposes of the endowment.

45 Waqf management: Inalienability and Istibdal The waqf asset may however be exchanged as an exception to the general rule of inalienability, when this is deemed to be in public interest. Such exchange or istibdal would however, require prior permission from the regulator with additional conditions that the same is (i) necessary or beneficial to the waqf; (ii) consistent with the objects of the waqf; (iii) against another asset of equal or higher value; (iv) and with due respect to the inalienability of religious awqaf. The issue of istabdal is explicitly dealt with by the law in Sudan (also in Indonesia) where the Diwan is empowered to sell an endowed asset to replace it with a better ones only to the extent deemed absolutely necessary.

46 Waqf Management: Lease of Assets Laws vary in permitting the trustee to lease out the property for varying periods governed by considerations of preservation as well as development. There is a need to ensure balance. Caps on lease period are as low as one-to-five years in Zanzibar; and three-to-nine years in Mauritius; ( 99 years in Singapore.)

47 Waqf Management: Public vs. Private Waqf is an institution originally and always meant to be in the voluntary sector with management of waqf entrusted to private parties. However, state has often sought to play a role in the ownership and management of awqaf, at times governed by motives to expropriate and at other times, by need to curb corrupt practices of private trusteemanagers. Positive evidence that the state can play the role of an efficient manager of awqaf with examples of large-scale development of existing awqaf in public-private mode (Sudan). Mixed evidence for public and private management in other countries.

48 Waqf Management: Private Laws must clearly articulate the responsibility of waqf management, that should not only emphasize preservation and protection of waqf assets, but also their development. The responsibility should also include transparent and honest reporting of financials. ( Mauritius)

49 Waqf Management: Incentivizing Private Management Law should adequately incentivize waqf management with clarity on remuneration (rewards) and punishment. In Mauritius, the remuneration to which a mutawalli/ nazir is entitled shall not exceed one tenth of the income Financial penalties, especially when these are expressed in absolute numbers tend to lose their effectiveness as deterrents with time (Mauritius).

50 Waqf Management: Investment Laws should explicitly deal with the issue of investment of waqf assets as investment can alone generate returns which may then be applied to the purpose for which the waqf has been created. Only the laws in Sudan and a few states in Nigeria include provisions relating to investments.

51 Waqf Management : Reforms Waqf legal and policy frameworks display wide variations. Reforms should take note of experiences and good practices in countries that have been more proactive in reforms. Reforms must seek to strike a balance between age-old ideas of preservation of awqaf rooted in perpetuity, inalienability of waqf and the development of awqaf through innovative private participation in the process.

52 Key Findings on IsMF Sector Enabling Environment Examples of Good Practices Islamic Research and Training Institute Member of the Islamic Development Bank Group

53 Enabling Environment IsMF Sector only Sudan has an Islamic microfinance system..docx other countries like Nigeria and Kenya are also included in this section for two reasons. Both Nigeria and Kenya have embarked on ambitious plans to strengthen their microfinance sectors and see microfinance as a tool of poverty alleviation. Nigeria additionally, has shown inclination to use Islamic modes, especially in its Northern states and therefore, the potential for Islamic microfinance in Nigeria is quite high. In Kenya, on other hand, there have been excellent examples of technology-driven microfinance. Islamic Research and Training Institute Member of the Islamic Development Bank Group

54 Enabling Environment IsMF Sector Sudan: The MFIs are guided by the regulatory framework of The regulatory framework covers MFIs, but the CBoS also give directives and annual policies for banks to extend MF in a certain ratio out of total bank's portfolio to MF clients (In 2008 CBoS financing policies directed banks to allocate at lease 12% of banking portfolio to MF.) Nigeria: The fact that microfinance in Nigeria was largely informal, in 2005, the government through the apex bank and based on provisions of Section 28, sub-section (1) (b) of the CBN Act 24 of 1991 (as amended) and in pursuance of the provisions of Sections 56-60(a) of the Bank and Other Financial Institutions Act (BOFIA) 25 of 1991 (as amended) releases microfinance Policy, Regulatory and Supervisory Framework for Nigeria. This was revised in April, 2011 to strengthen the policy. Kenya:Microfinance in Kenya is regulated under the Microfinance Act (2006) and the Microfinance Regulations (2008). These two sets of legislation define the legal, regultory and supervisory framework for the microfinance industry.

55 Good practices and policy Guidelines Report covers success stories and good practices. Al Hayat Relief Foundation, Nigeria Al-Anaam Microfinance, Sudan The microfinance program of Bank of Khartoum, known as IRADA,

56 Good Practices for IsMf Sector Islamic microfinance is seen as a solution to the challenge of self-exclusion. IsMFIs believe that they must play the role of an anchor and a facilitator in a process of transformation, and in the economic and social empowerment of the farming communities. They prefer to adopt a project approach and provide support in a multitude of areas other than finance, such as, technology, production, marketing, business development, capacity building, and thus, ultimately steering the project to success. Sudan provides interesting cases of both types of interventions. Islamic Research and Training Institute Member of the Islamic Development Bank Group

57 A review of various Islamic modes that are used for provision of finance to farmers reveals that there is no one-sizefits-all mode. even though bai salam is widely seen to be the appropriate mode for agricultural finance. Further, Shariahcompliance of a mode does not by itself ensure freedom from exploitation. As the examples show, salam can often involve exploitation when the advance price paid to the poor farmer is artificially pegged at low levels due to his/her weak bargaining power. Similarly, rates on murabaha and ijara financing can be and often are exploitatively high,could be unfairly biased against the poor beneficiary because of their low bargaining power. Prudential regulation of markets is an important pre-condition to ensure healthy and adequate competition among the players and thereby, remove abnormal and/or illegal profits through mispricing.

58 Good Practices for IsMf Sector In the Islamic approach, debt is not just discouraged; there are built-in mechanisms, such as zakat to address over-indebtedness of an individual. The paper documents the cases in Sudan where an institutional mechanism exists for use of zakat for curbing indebtedness. Islamic finance requires simplicity in contracts where the rights and obligations of the parties are well understood by them. The diminishing musharaka based models used in Sudan are apparently complex but quite definitive in terms of transfer of ownership of the key assets into the hands of farmers over a finite period.

59 Good Practices for IsMF Sector Poor farmers often require financial and a wide range of non-financial services. The case studies document a range of such services provided in Sudan including: technical assistance, skill enhancement, procurement, production, warehousing, processing, packaging and marketing support that underlies the success of these interventions. A related question is how these non-financial services are to be funded. Should they be priced? Should the farmers pay for these services? In the Sudanese examples, the costs are duly accounted for in the determination of profit-share for the farmers, while the contribution by the Ministry helps absorb certain costs. Importance of providing for basic consumption needs can not be ignored. Indeed, in case of the Sudanese projects the provision of safety net by IRADA is perhaps a significant contributor to the success of the projects.

60 Islamic Research and Training Institute Member of the Islamic Development Bank Group THANK YOU

61 15 June

62 Contacts of the presenter Contacts of IRTI Website: Phone: +966 (0) Fax: +966 (0) P.O. BOX Jeddah Kingdom of Saudi Arabia 15 June

Islam & Welfare State: Reality Check & The Way Forward

Islam & Welfare State: Reality Check & The Way Forward S A L M A N A H M E D S H A I K H P H D S C H O L A R I N E C O N O M I C S U N I V E R S I T I K E B A N G S A A N M A L A Y S I A S A L M A N @

Islam & Welfare State: Reality Check & The Way Forward S A L M A N A H M E D S H A I K H P H D S C H O L A R I N E C O N O M I C S U N I V E R S I T I K E B A N G S A A N M A L A Y S I A S A L M A N @

Zakat in Sudan Alamin Ali Abdelgadir, General director of Information center at Zakat Chamber

Zakat in Sudan Alamin Ali Abdelgadir, General director of Information center at Zakat Chamber Zakat is one of the pillars of Islam, taken from adult Muslim who owns wealth over a certain amount known as

Zakat in Sudan Alamin Ali Abdelgadir, General director of Information center at Zakat Chamber Zakat is one of the pillars of Islam, taken from adult Muslim who owns wealth over a certain amount known as

Establishment IDB Group

www.irti.org Establishment IDB Group Established 1981 Established 2008 Established 1975 Established 1994 Source: IRTI Annual Report Established 1999 Islamic Research and Training Institute Successful Islamic

www.irti.org Establishment IDB Group Established 1981 Established 2008 Established 1975 Established 1994 Source: IRTI Annual Report Established 1999 Islamic Research and Training Institute Successful Islamic

REQUIRED DOCUMENT FROM HIRING UNIT

Terms of reference GENERAL INFORMATION Title: Consultant for Writing on the Proposal of Zakat Trust Fund (International Consultant) Project Name: Social and Islamic Finance Reports to: Deputy Country Director,

Terms of reference GENERAL INFORMATION Title: Consultant for Writing on the Proposal of Zakat Trust Fund (International Consultant) Project Name: Social and Islamic Finance Reports to: Deputy Country Director,

BY-LAWS FIRST UNITED METHODIST CHURCH FOUNDATION MARION, IOWA I. STATEMENT OF PURPOSE AND INTENTION

BY-LAWS FIRST UNITED METHODIST CHURCH FOUNDATION MARION, IOWA I. STATEMENT OF PURPOSE AND INTENTION A. Statement of Purpose. The First United Methodist Church Foundation (hereinafter "the Foundation")

BY-LAWS FIRST UNITED METHODIST CHURCH FOUNDATION MARION, IOWA I. STATEMENT OF PURPOSE AND INTENTION A. Statement of Purpose. The First United Methodist Church Foundation (hereinafter "the Foundation")

WSS GSG UTILITY TURNAROUND SERIES. Population covered: 284,072 inhabitants for water

Public Disclosure Authorized Public Disclosure Authorized WATER GLOBAL PRACTICE Case Study PDAM Intan Banjar, Indonesia Alizar Anwar and Maria Salvetti AUGUST 2017 Key Characteristics of Aggregation Case

Public Disclosure Authorized Public Disclosure Authorized WATER GLOBAL PRACTICE Case Study PDAM Intan Banjar, Indonesia Alizar Anwar and Maria Salvetti AUGUST 2017 Key Characteristics of Aggregation Case

Islamic Microfinance 4th - 6th June, 2013 in Addis Ababa - Ethiopia

3 Days Specialized Training Workshop on Islamic Microfinance 4th - 6th June, 2013 in Addis Ababa - Ethiopia Jointly Organized By AlHuda Center of Excellence in Islamic Microfinance Islamic Microfinance

3 Days Specialized Training Workshop on Islamic Microfinance 4th - 6th June, 2013 in Addis Ababa - Ethiopia Jointly Organized By AlHuda Center of Excellence in Islamic Microfinance Islamic Microfinance

Islamic Finance in ending poverty & fighting inequalities: Indonesia experiences. IDB Global Forum on Islamic Finance Jakarta, 16 th May 2016

1 Islamic Finance in ending poverty & fighting inequalities: Indonesia experiences IDB Global Forum on Islamic Finance Jakarta, 16 th May 2016 Foreword 2 This presentation will focus on the segment of

1 Islamic Finance in ending poverty & fighting inequalities: Indonesia experiences IDB Global Forum on Islamic Finance Jakarta, 16 th May 2016 Foreword 2 This presentation will focus on the segment of

Technical Release i -1. Accounting for Zakat on Business

LEMBAGA PIAWAIAN PERAKAUNAN MALAYSIA MALAYSIAN ACCOUNTING STANDARDS BOARD Technical Release i -1 Accounting for Zakat on Business Malaysian Accounting Standards Board 2006 1 Accounting for Zakat on Business

LEMBAGA PIAWAIAN PERAKAUNAN MALAYSIA MALAYSIAN ACCOUNTING STANDARDS BOARD Technical Release i -1 Accounting for Zakat on Business Malaysian Accounting Standards Board 2006 1 Accounting for Zakat on Business

Zakat & Waqf Institutions

Sharia Implementation in Northern Nigeria Over 15 Years. Policy Brief No.3 Zakat & Waqf Institutions 3 Zakat & Waqf Institutions. 1 Background The return of Nigeria to democratic governance on May 29,

Sharia Implementation in Northern Nigeria Over 15 Years. Policy Brief No.3 Zakat & Waqf Institutions 3 Zakat & Waqf Institutions. 1 Background The return of Nigeria to democratic governance on May 29,

ISLAMIC FINANCE PROGRAMMES

ISLAMIC FINANCE PROGRAMMES BANKING ACCOUNTING & FINANCE ISLAMIC FINANCE IT & PROJECT MANAGEMENT INSURANCE LEADERSHIP & MANAGEMENT EXECUTIVE LEADERSHIP ACADEMIC STUDIES ABOUT The BIBF is a semi-government

ISLAMIC FINANCE PROGRAMMES BANKING ACCOUNTING & FINANCE ISLAMIC FINANCE IT & PROJECT MANAGEMENT INSURANCE LEADERSHIP & MANAGEMENT EXECUTIVE LEADERSHIP ACADEMIC STUDIES ABOUT The BIBF is a semi-government

Islamic Microfinance an incredible tool to Alleviate Poverty!

Islamic Microfinance an incredible tool to Alleviate Poverty! AlHuda Center of Excellence in Islamic Microfinance is an initiative of AlHuda CIBE. AlHuda CIBE is a well established name in Islamic financial

Islamic Microfinance an incredible tool to Alleviate Poverty! AlHuda Center of Excellence in Islamic Microfinance is an initiative of AlHuda CIBE. AlHuda CIBE is a well established name in Islamic financial

INSTITUTE OF HAZRAT MOHAMMAD (SAW)

") INNOVATIONS IN ISLAMIC PHILANTHROPY AND MONETIZATION OF ISLAMIC PHILANTHOROPIC INSTRUMENTS by Tanim Laila Director Institute of Hazrat Mohammad (SAW) INSTITUTE OF HAZRAT MOHAMMAD (SAW) House- 22, Road-

INNOVATIONS IN ISLAMIC PHILANTHROPY AND MONETIZATION OF ISLAMIC PHILANTHOROPIC INSTRUMENTS by Tanim Laila Director Institute of Hazrat Mohammad (SAW) INSTITUTE OF HAZRAT MOHAMMAD (SAW) House- 22, Road-

Welfare Potential of Zakat: An Attempt to Estimate Economy wide Zakat Collection

Welfare Potential of Zakat: An Attempt to Estimate Economy wide Zakat Collection S A L M A N A H M E D S H A I K H P H D S C H O L A R I N E C O N O M I C S I S L A M I C E C O N O M I C S P R O J E C

Welfare Potential of Zakat: An Attempt to Estimate Economy wide Zakat Collection S A L M A N A H M E D S H A I K H P H D S C H O L A R I N E C O N O M I C S I S L A M I C E C O N O M I C S P R O J E C

th th July, 2018 Nairobi - Kenya

th th 27-28 July, 2018 Nairobi - Kenya www.alhudacibe.com CIBE ALHUDA CENTER OF ISLAMIC BANKING AND ECONOMICS AlHuda Center of Islamic Banking and Economics (CIBE) is a pioneer organization started its

th th 27-28 July, 2018 Nairobi - Kenya www.alhudacibe.com CIBE ALHUDA CENTER OF ISLAMIC BANKING AND ECONOMICS AlHuda Center of Islamic Banking and Economics (CIBE) is a pioneer organization started its

The Experience of Islamic Banking in a Conventional System

The Experience of Islamic Banking in a Conventional System A Country Case study: Morocco Dr. Amal Smaili, Netherlands The Second Annual Conference of Islamic Economics & Islamic Finance Venue: Chestnut

The Experience of Islamic Banking in a Conventional System A Country Case study: Morocco Dr. Amal Smaili, Netherlands The Second Annual Conference of Islamic Economics & Islamic Finance Venue: Chestnut

Towards Institutional Mutawallis for the Management of Waqf Properties

Towards Institutional Mutawallis for the Management of Waqf Properties Dr. Muhammad Yusuf Saleem Department of Economics Faculty of Economics and Management Sciences International Islamic University Malaysia

Towards Institutional Mutawallis for the Management of Waqf Properties Dr. Muhammad Yusuf Saleem Department of Economics Faculty of Economics and Management Sciences International Islamic University Malaysia

Challenges in Islamic Finance

Challenges in Islamic Finance Dr. Ahmet Sekreter Business and Management Department, Ishik University, Erbil, Iraq Email: ahmet.sekreter@ishik.edu.iq Abstract Doi:10.23918/icabep2018p29 The growth of Islamic

Challenges in Islamic Finance Dr. Ahmet Sekreter Business and Management Department, Ishik University, Erbil, Iraq Email: ahmet.sekreter@ishik.edu.iq Abstract Doi:10.23918/icabep2018p29 The growth of Islamic

1. After a public profession of faith in Christ as personal savior, and upon baptism by immersion in water as authorized by the Church; or

BYLAWS GREEN ACRES BAPTIST CHURCH OF TYLER, TEXAS ARTICLE I MEMBERSHIP A. THE MEMBERSHIP The membership of Green Acres Baptist Church, Tyler, Texas, referred to herein as the "Church, will consist of all

BYLAWS GREEN ACRES BAPTIST CHURCH OF TYLER, TEXAS ARTICLE I MEMBERSHIP A. THE MEMBERSHIP The membership of Green Acres Baptist Church, Tyler, Texas, referred to herein as the "Church, will consist of all

Sharia Implementation in Northern Nigeria Over 15 Years. Policy Brief No.3. Zakat & Waqf

Sharia Implementation in Northern Nigeria Over 15 Years. Policy Brief No.3 Zakat & Waqf 3 Zakat & Waqf. 1 Introduction The return of Nigeria to democratic governance on May 29, 1999, reinvigorated the

Sharia Implementation in Northern Nigeria Over 15 Years. Policy Brief No.3 Zakat & Waqf 3 Zakat & Waqf. 1 Introduction The return of Nigeria to democratic governance on May 29, 1999, reinvigorated the

Islamic Microfinance An Incredible Tool to Alleviate Poverty

Islamic Microfinance An Incredible Tool to Alleviate Poverty AlHuda CIBE is now firmly established in Islamic Financial market, working in the field of Islamic Banking & Finance for the last seven years

Islamic Microfinance An Incredible Tool to Alleviate Poverty AlHuda CIBE is now firmly established in Islamic Financial market, working in the field of Islamic Banking & Finance for the last seven years

List of Figures. List of Tables. Acknowledgements. About the Author. About the Website

Contents List of Figures List of Tables Acknowledgements About the Author Preface About the Website CHAPTER 1 Introduction to Islamic Finance and Islamic Economics 1 Introduction 1 Creation of Money and

Contents List of Figures List of Tables Acknowledgements About the Author Preface About the Website CHAPTER 1 Introduction to Islamic Finance and Islamic Economics 1 Introduction 1 Creation of Money and

The 6th Azerbaijan Micro-finance Conference

The 6th Azerbaijan Micro-finance Conference 3 Days Post Event Training Workshop on Islamic Microfinance (Including Islamic Banking, Islamic Finance and Islamic Insurance) 8th 10th October, 2012 in Baku

The 6th Azerbaijan Micro-finance Conference 3 Days Post Event Training Workshop on Islamic Microfinance (Including Islamic Banking, Islamic Finance and Islamic Insurance) 8th 10th October, 2012 in Baku

things things FIRST FIRST FIRST FIRST

Martin Luther once observed that every Christian goes through three conversions in life---first, the heart, then, the head, and finally the purse. For God to be really first in the life of a Christian,

Martin Luther once observed that every Christian goes through three conversions in life---first, the heart, then, the head, and finally the purse. For God to be really first in the life of a Christian,

Application of Waqf as Social Safety Net & Public Infrastructure Financing. Salman Ahmed Shaikh Dr. Abdul Ghafar Ismail Dr.

Application of Waqf as Social Safety Net & Public Infrastructure Financing Salman Ahmed Shaikh Dr. Abdul Ghafar Ismail Dr. Bayu Taufiq Application of Waqf as Social Safety Net & Public Infrastructure Financing

Application of Waqf as Social Safety Net & Public Infrastructure Financing Salman Ahmed Shaikh Dr. Abdul Ghafar Ismail Dr. Bayu Taufiq Application of Waqf as Social Safety Net & Public Infrastructure Financing

Assessment on the Willingness among Public in Contributing For Social Islamic Waqf Bank for Education

AENSI Journals Australian Journal of Basic and Applied Sciences Journal home page: www.ajbasweb.com Assessment on the Willingness among Public in Contributing For Social Islamic Waqf Bank for Education

AENSI Journals Australian Journal of Basic and Applied Sciences Journal home page: www.ajbasweb.com Assessment on the Willingness among Public in Contributing For Social Islamic Waqf Bank for Education

One Day Specialized Training on Islamic Banking, Finance and Islamic Microfinance

One Day Specialized Training on Islamic Banking, Finance and Islamic Microfinance th 19 January, 2018 Sofitel Hotel, Manila Philippines. ALHUDA CENTER OF ISLAMIC BANKING AND ECONOMICS AlHuda Center of

One Day Specialized Training on Islamic Banking, Finance and Islamic Microfinance th 19 January, 2018 Sofitel Hotel, Manila Philippines. ALHUDA CENTER OF ISLAMIC BANKING AND ECONOMICS AlHuda Center of

Project 1: Grameen Foundation USA, Philippine Microfinance Initiative

These sample project descriptions illustrate the typical scope and level of depth used to solicit student applications. Project descriptions should be submitted using IDC_Client_Application_Form.doc. Project

These sample project descriptions illustrate the typical scope and level of depth used to solicit student applications. Project descriptions should be submitted using IDC_Client_Application_Form.doc. Project

Serving Muslim Clients. A very brief introduction to Islamic Finance

Serving Muslim Clients A very brief introduction to Islamic Finance History of Islamic finance Not New 1500 years of development. During Classical period, commerce flourished under Islamic commercial law.

Serving Muslim Clients A very brief introduction to Islamic Finance History of Islamic finance Not New 1500 years of development. During Classical period, commerce flourished under Islamic commercial law.

Seminars Organization

Seminars Organization Trainings/Seminars Title and Duration, please select the suitable by marking (x): No. Title Duration Hours Selection Exam. Yes No 1 The General Islamic Banking 3 days 15 hours 2 The

Seminars Organization Trainings/Seminars Title and Duration, please select the suitable by marking (x): No. Title Duration Hours Selection Exam. Yes No 1 The General Islamic Banking 3 days 15 hours 2 The

Establishing Economies According to Islamic Worldview: Problems and Way Forward. Prof. Habib Ahmed Durham University

Establishing Economies According to Islamic Worldview: Problems and Way Forward Prof. Habib Ahmed Durham University Presentation Plan Islamic Economics: Ideals and Reality New Institutional Economics (NIE)

Establishing Economies According to Islamic Worldview: Problems and Way Forward Prof. Habib Ahmed Durham University Presentation Plan Islamic Economics: Ideals and Reality New Institutional Economics (NIE)

Financing Climate Change Project: Beyond Conventional Scheme Case of Jakarta

Financing Climate Change Project: Beyond Conventional Scheme Case of Jakarta Oswar Mungkasa Deputy Governor of Jakarta for Spatial Planning and Environment Panel Financing Adaptation Projects in Cities

Financing Climate Change Project: Beyond Conventional Scheme Case of Jakarta Oswar Mungkasa Deputy Governor of Jakarta for Spatial Planning and Environment Panel Financing Adaptation Projects in Cities

WAQF AND ITS ROLE IN SOCIO- ECONOMIC DEVELOPMENT

WAQF AND ITS ROLE IN SOCIO- ECONOMIC DEVELOPMENT Mazrul Shahir Md Zuki* I. INTRODUCTION Waqf is an important institution in the Islamic socio-economic system. It has played a key role throughout Islamic

WAQF AND ITS ROLE IN SOCIO- ECONOMIC DEVELOPMENT Mazrul Shahir Md Zuki* I. INTRODUCTION Waqf is an important institution in the Islamic socio-economic system. It has played a key role throughout Islamic

The United Reformed Church Northern Synod

The United Reformed Church Northern Synod Guidelines and Procedures on the Care of Manses In recent years, many synods have introduced a variety of manse policies. In 2009, a task group was set up in Northern

The United Reformed Church Northern Synod Guidelines and Procedures on the Care of Manses In recent years, many synods have introduced a variety of manse policies. In 2009, a task group was set up in Northern

23 September, 2017, Manila - Philippine

23 September, 2017, Manila - Philippine Registered with FAA as Training Provider ALHUDA CENTER OF ISLAMIC BANKING AND ECONOMICS AlHuda Center of Islamic Banking and Economics (CIBE) is a pioneer organization

23 September, 2017, Manila - Philippine Registered with FAA as Training Provider ALHUDA CENTER OF ISLAMIC BANKING AND ECONOMICS AlHuda Center of Islamic Banking and Economics (CIBE) is a pioneer organization

Towards a Sustainable Islamic Microfinance Model in Pakistan

Journal of Islamic Banking and Finance Julyl Sept 2016 1 Towards a Sustainable Islamic Microfinance Model in Pakistan Salman Ahmed Shaikh According to SDPI estimates, poverty rate in Pakistan has increased

Journal of Islamic Banking and Finance Julyl Sept 2016 1 Towards a Sustainable Islamic Microfinance Model in Pakistan Salman Ahmed Shaikh According to SDPI estimates, poverty rate in Pakistan has increased

7th GLOBAL Islamic Microfinance Forum

7th GLOBAL Islamic Microfinance Forum 24-25 November 2017 Istanbul, Turkey Advocating for an Enabling Framework on Islamic Microfinance and a Mechanism for Zakat to Accelerate Genuine and Sustainable Rehabilitation

7th GLOBAL Islamic Microfinance Forum 24-25 November 2017 Istanbul, Turkey Advocating for an Enabling Framework on Islamic Microfinance and a Mechanism for Zakat to Accelerate Genuine and Sustainable Rehabilitation

Technical Committee of Experts on Islamic Banking and Finance. Third Session of OIC Statistical Commission April 2013 Ankara - Turkey

Technical Committee of Experts on Islamic Banking and Finance Third Session of OIC Statistical Commission 10-12 April 2013 Ankara - Turkey BACKGROUND Owing to the increasing importance of the role of statistics

Technical Committee of Experts on Islamic Banking and Finance Third Session of OIC Statistical Commission 10-12 April 2013 Ankara - Turkey BACKGROUND Owing to the increasing importance of the role of statistics

World Cultures and Geography

McDougal Littell, a division of Houghton Mifflin Company correlated to World Cultures and Geography Category 2: Social Sciences, Grades 6-8 McDougal Littell World Cultures and Geography correlated to the

McDougal Littell, a division of Houghton Mifflin Company correlated to World Cultures and Geography Category 2: Social Sciences, Grades 6-8 McDougal Littell World Cultures and Geography correlated to the

The AEG is requested to: Provide guidance on the recommendations presented in paragraphs of the issues paper.

SNA/M1.17/5.1 11th Meeting of the Advisory Expert Group on National Accounts, 5-7 December 2017, New York, USA Agenda item: 5.1 Islamic finance in the national accounts Introduction The 10 th meeting of

SNA/M1.17/5.1 11th Meeting of the Advisory Expert Group on National Accounts, 5-7 December 2017, New York, USA Agenda item: 5.1 Islamic finance in the national accounts Introduction The 10 th meeting of

Organizational Bylaws July Deer Creek Rd. Monument, CO 80132

Organizational Bylaws July 2016 1750 Deer Creek Rd. Monument, CO 80132 2 ARTICLE I NAME The name of this church is The Ascent Church. ARTICLE II MISSION OF THE ASCENT CHURCH Our mission focuses on Jesus

Organizational Bylaws July 2016 1750 Deer Creek Rd. Monument, CO 80132 2 ARTICLE I NAME The name of this church is The Ascent Church. ARTICLE II MISSION OF THE ASCENT CHURCH Our mission focuses on Jesus

CHAPTER V CONCLUSION & SUGGESTION. broaden its effect, program on zakat microfinance is a smart step. Assessment and

CHAPTER V CONCLUSION & SUGGESTION 5.1. Conclusion Zakat multiplier effect on economy is no doubt. To accelerate and broaden its effect, program on zakat microfinance is a smart step. Assessment and evaluation

CHAPTER V CONCLUSION & SUGGESTION 5.1. Conclusion Zakat multiplier effect on economy is no doubt. To accelerate and broaden its effect, program on zakat microfinance is a smart step. Assessment and evaluation

SUKUK a main financial tool funding terror Introduction

SUKUK a main financial tool funding terror Introduction Sukuk is an Islamic financial certificate, similar to a bond in Western finance, that complies with Sharia, Islamic religious law. Because the traditional

SUKUK a main financial tool funding terror Introduction Sukuk is an Islamic financial certificate, similar to a bond in Western finance, that complies with Sharia, Islamic religious law. Because the traditional

Law of the Russian Soviet Federative Socialist Republic on Freedom of Worship (25/10/1990)

") Law of the Russian Soviet Federative Socialist Republic on Freedom of Worship (25/10/1990) I. GENERAL PROVISIONS Article 1. The Purpose of This Law The purpose of the Law of the RSFSR on Freedom of Worship

Law of the Russian Soviet Federative Socialist Republic on Freedom of Worship (25/10/1990) I. GENERAL PROVISIONS Article 1. The Purpose of This Law The purpose of the Law of the RSFSR on Freedom of Worship

Resolution of OIC Fiqh Academy (related to Islamic Economic and Finance) بسم هللا الرحمن الرحيم

بسم هللا الرحمن الرحيم") Islamic Economic Studies Vol. 22, No. 1, May, 2014 DOI No. 10.12816/0004141 Resolution of OIC Fiqh Academy (related to Islamic Economic and Finance) بسم هللا الرحمن الرحيم Resolution 188 (3/20) Completion

Islamic Economic Studies Vol. 22, No. 1, May, 2014 DOI No. 10.12816/0004141 Resolution of OIC Fiqh Academy (related to Islamic Economic and Finance) بسم هللا الرحمن الرحيم Resolution 188 (3/20) Completion

ww.fidfinvest.com Islamic Finance an Introduction

Islamic Finance an Introduction Islamic a word, which nowadays puts many people on alert, in particular, those who regularly watch certain media, and thus develop a kind of what is called Islamophobia

Islamic Finance an Introduction Islamic a word, which nowadays puts many people on alert, in particular, those who regularly watch certain media, and thus develop a kind of what is called Islamophobia

Bill Cochran Lutheran Elementary Schools: Opportunities and Challenges

Bill Cochran Lutheran Elementary Schools: Opportunities and Challenges Illustration by Michelle Roeber 16 Issues Spring 2008 Therefore let all Israel be assured of this: God has made this Jesus, whom you

Bill Cochran Lutheran Elementary Schools: Opportunities and Challenges Illustration by Michelle Roeber 16 Issues Spring 2008 Therefore let all Israel be assured of this: God has made this Jesus, whom you

Brochure of Robin Jeffs Registered Investment Advisor CRD # Ashdown Place Half Moon Bay, CA Telephone (650)

") Item 1. Cover Page Brochure of Robin Jeffs Registered Investment Advisor CRD #136030 6 Ashdown Place Half Moon Bay, CA 94019 Telephone (650) 712-8591 rjeffs@comcast.net May 27, 2011 This brochure provides

Item 1. Cover Page Brochure of Robin Jeffs Registered Investment Advisor CRD #136030 6 Ashdown Place Half Moon Bay, CA 94019 Telephone (650) 712-8591 rjeffs@comcast.net May 27, 2011 This brochure provides

Presentation Coverage

www.irti.org Presentation Coverage 1 IRTI Products and Services 2 Islamic Finance Sustainable Development 3 Benefits of Islamic Financial Institutions 4 Benefits of Sukuk Source: IRTI database Islamic

www.irti.org Presentation Coverage 1 IRTI Products and Services 2 Islamic Finance Sustainable Development 3 Benefits of Islamic Financial Institutions 4 Benefits of Sukuk Source: IRTI database Islamic

THE PRESBYTERIAN HUNGER PROGRAM

THE PRESBYTERIAN HUNGER PROGRAM HOW IT WORKS IN RESPONDING TO WORLD HUNGER THE COMMON AFFIRMATION ON GLOBAL HUNGER In 1979 the General Assemblies of the two predecessors of the Presbyterian Church (USA)

THE PRESBYTERIAN HUNGER PROGRAM HOW IT WORKS IN RESPONDING TO WORLD HUNGER THE COMMON AFFIRMATION ON GLOBAL HUNGER In 1979 the General Assemblies of the two predecessors of the Presbyterian Church (USA)

and sexuality, a local church or annual conference may indicate its desire to form or join a self-governing

Total Number of Pages: 14 Suggested Title: Modified Traditional Plan - Traditional Plan Implementation Process Discipline Paragraph or Resolution Number, if applicable: Discipline New 2801 General Church

Total Number of Pages: 14 Suggested Title: Modified Traditional Plan - Traditional Plan Implementation Process Discipline Paragraph or Resolution Number, if applicable: Discipline New 2801 General Church

Analysis of Minor Proposals outside the Mainstream Islamic Finance in Pakistan

Journal of Islamic Banking and Finance July Sept 2017 1 Analysis of Minor Proposals outside the Mainstream Islamic Finance in Pakistan Salman Ahmed Shaikh This paper is a humble attempt to discuss the

Journal of Islamic Banking and Finance July Sept 2017 1 Analysis of Minor Proposals outside the Mainstream Islamic Finance in Pakistan Salman Ahmed Shaikh This paper is a humble attempt to discuss the

MODERNISATION STRATEGIES ON COLLECTION AND DISTRIBUTION OF ZAKAT

MODERNISATION STRATEGIES ON COLLECTION AND DISTRIBUTION OF ZAKAT Challenges 1. Low level of public confidence 2. the need to introduce more effective channel of payment 3. Lack of aggressive efforts in

MODERNISATION STRATEGIES ON COLLECTION AND DISTRIBUTION OF ZAKAT Challenges 1. Low level of public confidence 2. the need to introduce more effective channel of payment 3. Lack of aggressive efforts in

Building community, shaping leaders

Annual Report 2011 Building community, shaping leaders To support the preparation of church leaders, Luther Seminary s Olson Campus Center underwent a major reconstruction project. The renovation was made

Annual Report 2011 Building community, shaping leaders To support the preparation of church leaders, Luther Seminary s Olson Campus Center underwent a major reconstruction project. The renovation was made

The Islamic Finance Qualification (IFQ) expands upon knowledge gained from the Fundamentals of Islamic Banking and Finance.

expands upon knowledge gained from the Fundamentals of Islamic Banking and Finance.") The Islamic Finance Qualification (IFQ) expands upon knowledge gained from the Fundamentals of Islamic Banking and Finance. It is a global qualification that covers Islamic finance from both a technical

The Islamic Finance Qualification (IFQ) expands upon knowledge gained from the Fundamentals of Islamic Banking and Finance. It is a global qualification that covers Islamic finance from both a technical

Peddling Religion? What is Islamic Finance? & Should we support it?

Peddling Religion? What is Islamic Finance? & Should we support it? Mahmoud A. El-Gamal Rice University Is there an Islamic Finance? All financial products available today are suspect : Mortgages, and

Peddling Religion? What is Islamic Finance? & Should we support it? Mahmoud A. El-Gamal Rice University Is there an Islamic Finance? All financial products available today are suspect : Mortgages, and

Resolution of OIC Fiqh Academy (related to Islamic Economic and Finance) بسم هللا الرحمن الرحيم

بسم هللا الرحمن الرحيم") Islamic Economic Studies Vol. 20, No.1, June 2012 Resolution of OIC Fiqh Academy (related to Islamic Economic and Finance) بسم هللا الرحمن الرحيم Resolution 165(18/3) on Activation of the Role of Zak t

Islamic Economic Studies Vol. 20, No.1, June 2012 Resolution of OIC Fiqh Academy (related to Islamic Economic and Finance) بسم هللا الرحمن الرحيم Resolution 165(18/3) on Activation of the Role of Zak t

Sources of Financing Funding

Sources of Financing Funding Activities Sheikh Mufti Mohammed Zubair Butt Shariah Advisor, Halal Monitoring Committee, United Kingdom The First Gulf Workshop on the Halal Industry and its Services 27-28

Sources of Financing Funding Activities Sheikh Mufti Mohammed Zubair Butt Shariah Advisor, Halal Monitoring Committee, United Kingdom The First Gulf Workshop on the Halal Industry and its Services 27-28

CERTIFICATE IN ISLAMIC BANKING AND FINANCE

CERTIFICATE IN ISLAMIC BANKING AND FINANCE INTRODUCTION Islamic Finance refers to the provision of financial services in accordance with the Shari ah Islamic law, principles and rules. Shari ah does not

CERTIFICATE IN ISLAMIC BANKING AND FINANCE INTRODUCTION Islamic Finance refers to the provision of financial services in accordance with the Shari ah Islamic law, principles and rules. Shari ah does not

MEMBERSHIP & PARTICIPATION Table 1 of the Local Church Report to the Annual Conference

State County Charge Conference Church No. GCFA Church No. Employer Identification No. (Federal Tax ID No.) Pastor Church District Reports for the year ending December 31, or for the period to Mission Church

State County Charge Conference Church No. GCFA Church No. Employer Identification No. (Federal Tax ID No.) Pastor Church District Reports for the year ending December 31, or for the period to Mission Church

MISSIONS POLICY THE HEART OF CHRIST CHURCH SECTION I INTRODUCTION

MISSIONS POLICY THE HEART OF CHRIST CHURCH SECTION I INTRODUCTION A. DEFINITION OF MISSIONS Missions shall be understood as any Biblically supported endeavor to fulfill the Great Commission of Jesus Christ,

MISSIONS POLICY THE HEART OF CHRIST CHURCH SECTION I INTRODUCTION A. DEFINITION OF MISSIONS Missions shall be understood as any Biblically supported endeavor to fulfill the Great Commission of Jesus Christ,

LOCAL CHURCH REPORT TO THE ANNUAL CONFERENCE

Instructions for Table I of the 1 This is auto-filled from Line 9 of last year s Local Church Report. 2.a Report the number of persons received into the church on profession of faith. 2.b Report the number

Instructions for Table I of the 1 This is auto-filled from Line 9 of last year s Local Church Report. 2.a Report the number of persons received into the church on profession of faith. 2.b Report the number

World Church Financial Update March 2018

World Church Financial Update March 2018 IN THIS UPDATE 1. 2017 Worldwide Mission Tithes: Thank You! Together We re Financially Supporting Worldwide Mission 2. Fiscal Year 2017: Improved Net Asset Position

World Church Financial Update March 2018 IN THIS UPDATE 1. 2017 Worldwide Mission Tithes: Thank You! Together We re Financially Supporting Worldwide Mission 2. Fiscal Year 2017: Improved Net Asset Position

THE ROLE OF CENTRAL BANK OF MALAYSIA IN DEVELOPING MALAYSIA'S ISLAMIC FINANCIAL INDUSTRY

الا كاديمية العالمية للبحوث الشرعية ISRA International Shari ah Research Academy for Islamic Finance THE ROLE OF CENTRAL BANK OF MALAYSIA IN DEVELOPING MALAYSIA'S ISLAMIC FINANCIAL INDUSTRY Prof. Dr. Mohamad

الا كاديمية العالمية للبحوث الشرعية ISRA International Shari ah Research Academy for Islamic Finance THE ROLE OF CENTRAL BANK OF MALAYSIA IN DEVELOPING MALAYSIA'S ISLAMIC FINANCIAL INDUSTRY Prof. Dr. Mohamad

Overview of Islamic Banking & Islamic Finance in Morocco. Dr. Ahmed TAHIRI JOUTI

Overview of Islamic Banking & Islamic Finance in Morocco Dr. Ahmed TAHIRI JOUTI Overview of Islamic Banking & Islamic Finance in Morocco This presentation gives a general overview of the Moroccan experience

Overview of Islamic Banking & Islamic Finance in Morocco Dr. Ahmed TAHIRI JOUTI Overview of Islamic Banking & Islamic Finance in Morocco This presentation gives a general overview of the Moroccan experience

Evangelical Lutheran Church in Canada Congregational Mission Profile

Evangelical Lutheran Church in Canada Congregational Mission Profile Part I Congregation Information 1. Congregation Congregation ID Number: Date Submitted: Congregation Name: Address: City: Postal Code:

Evangelical Lutheran Church in Canada Congregational Mission Profile Part I Congregation Information 1. Congregation Congregation ID Number: Date Submitted: Congregation Name: Address: City: Postal Code:

8th Azerbaijan Micro-finance Conference 2 Days Post Event Training Workshop on. Islamic Finance

8th Azerbaijan Micro-finance Conference 2 Days Post Event Training Workshop on Islamic Finance (including Islamic Microfinance, Islamic Insurance,Sukuk) 12th & 13th October,2015 in Baku - Azerbaijan Jointly

8th Azerbaijan Micro-finance Conference 2 Days Post Event Training Workshop on Islamic Finance (including Islamic Microfinance, Islamic Insurance,Sukuk) 12th & 13th October,2015 in Baku - Azerbaijan Jointly

Doug Swanney Connexional Secretary Graeme Hodge CEO of All We Can

Framework of Commitment with All We Can Contact Name and Details Status of Paper Action Required Resolution Doug Swanney Connexional Secretary swanneyd@methodistchurch.org.uk Graeme Hodge CEO of All We

Framework of Commitment with All We Can Contact Name and Details Status of Paper Action Required Resolution Doug Swanney Connexional Secretary swanneyd@methodistchurch.org.uk Graeme Hodge CEO of All We

Rudolf Böhmler Member of the Executive Board of the Deutsche Bundesbank. 2nd Islamic Financial Services Forum: The European Challenge

Rudolf Böhmler Member of the Executive Board of the Deutsche Bundesbank 2nd Islamic Financial Services Forum: The European Challenge Speech held at Frankfurt am Main Wednesday, 5 December 2007 Check against

Rudolf Böhmler Member of the Executive Board of the Deutsche Bundesbank 2nd Islamic Financial Services Forum: The European Challenge Speech held at Frankfurt am Main Wednesday, 5 December 2007 Check against

Used by DS s, Bishops, Conference and General Agency Staff, and Academic

# Name What is this for? Who uses it (beyond the local church)? 1 Total professing members reported at the close of last year Used by local churches, annual conferences, and GCFA for internal data auditing

# Name What is this for? Who uses it (beyond the local church)? 1 Total professing members reported at the close of last year Used by local churches, annual conferences, and GCFA for internal data auditing

Sustainability: Waqf and Zakat Contributions

Monash University Malaysia is jointly owned by Monash University and the Jeffrey Cheah Foundation Business Sustainability: Waqf and Zakat Contributions Presentation for the International Conference on

Monash University Malaysia is jointly owned by Monash University and the Jeffrey Cheah Foundation Business Sustainability: Waqf and Zakat Contributions Presentation for the International Conference on

BY-LAWS OF LIVING WATER COMMUNITY CHURCH ARTICLE I. NAME AND CORPORATE OFFICE SECTION A: NAME The name of this corporation is Living Water Community

BY-LAWS OF LIVING WATER COMMUNITY CHURCH ARTICLE I. NAME AND CORPORATE OFFICE SECTION A: NAME The name of this corporation is Living Water Community Church. SECTION B: CORPORATE OFFICE AND AGENT Living

BY-LAWS OF LIVING WATER COMMUNITY CHURCH ARTICLE I. NAME AND CORPORATE OFFICE SECTION A: NAME The name of this corporation is Living Water Community Church. SECTION B: CORPORATE OFFICE AND AGENT Living

The reality of the Islamic financing and its prospects of development in the Jordanian cities and villages development bank

2016; 2(12): 567-572 ISSN Print: 2394-7500 ISSN Online: 2394-5869 Impact Factor: 5.2 IJAR 2016; 2(12): 567-572 www.allresearchjournal.com Received: 23-10-2016 Accepted: 24-11-2016 Lena Hashem al-waked

2016; 2(12): 567-572 ISSN Print: 2394-7500 ISSN Online: 2394-5869 Impact Factor: 5.2 IJAR 2016; 2(12): 567-572 www.allresearchjournal.com Received: 23-10-2016 Accepted: 24-11-2016 Lena Hashem al-waked

CHARACTERISTICS THAT CAN DESCRIBE A SANGHA AS "GOOD"

MYRADA Rural Management Systems Series Paper - 15 2, Service Road Domlur Layout BANGALORE 560 071. INDIA. Fax E-mail Website : : : : 5353166, 5354457, 5352028, 5358279 091-80 - 5350982 myrada@blr.vsnl.net.in

MYRADA Rural Management Systems Series Paper - 15 2, Service Road Domlur Layout BANGALORE 560 071. INDIA. Fax E-mail Website : : : : 5353166, 5354457, 5352028, 5358279 091-80 - 5350982 myrada@blr.vsnl.net.in

Employment Agreement

Employment Agreement Ordained Minister THIS AGREEMENT MADE BETWEEN: (Name of the Congregation) (herein called Congregation ) OF THE FIRST PART, -and- (Name of the Ordained Minister) (herein called Ordained

Employment Agreement Ordained Minister THIS AGREEMENT MADE BETWEEN: (Name of the Congregation) (herein called Congregation ) OF THE FIRST PART, -and- (Name of the Ordained Minister) (herein called Ordained

M&SME ISLAMIC BANKING MASTERCLASS PACKAGEE

M&SME ISLAMIC BANKING MASTERCLASS PACKAGEE M&SME ISLAMIC BANKING MASTERCLASS PACKAGEE Islamic banks have been operating in places such as Bahrain, Saudi Arabia, Malaysia, Dubai and some Western Countries

M&SME ISLAMIC BANKING MASTERCLASS PACKAGEE M&SME ISLAMIC BANKING MASTERCLASS PACKAGEE Islamic banks have been operating in places such as Bahrain, Saudi Arabia, Malaysia, Dubai and some Western Countries

1. Be a committed Christian who, upon appointment, will become a member of Bendigo Baptist Church.

Bendigo Baptist Church (BBC) Administrator Position Description 2017 Mission & Vision: Our mission at BBC is to develop people into fully devoted followers of Jesus Christ. As we accomplish this, it s

Bendigo Baptist Church (BBC) Administrator Position Description 2017 Mission & Vision: Our mission at BBC is to develop people into fully devoted followers of Jesus Christ. As we accomplish this, it s

Prof. Habib Ahmed Durham University, UK

Prof. Habib Ahmed Durham University, UK Agenda Waqf: From Past to Present In Search for Efficiency Introduction The voluntary sector is increasingly playing an important role providing many social goods

Prof. Habib Ahmed Durham University, UK Agenda Waqf: From Past to Present In Search for Efficiency Introduction The voluntary sector is increasingly playing an important role providing many social goods

BY-LAWS. of the Islamic Community. of North American Bosniaks

BY-LAWS of the Islamic Community of North American Bosniaks 1 I NAME OF THE ORGANIZATION Article 1 The Islamic Community of Bosniaks is the highest religious community of all Bosniak Jamaats in North America

BY-LAWS of the Islamic Community of North American Bosniaks 1 I NAME OF THE ORGANIZATION Article 1 The Islamic Community of Bosniaks is the highest religious community of all Bosniak Jamaats in North America

Diocese of Saginaw Parish Finance Council Norms

Diocese of Saginaw Parish Finance Council Norms In each parish there is to be a finance council which is governed, in addition to universal law, by norms issued by the Diocesan Bishop and in which the

Diocese of Saginaw Parish Finance Council Norms In each parish there is to be a finance council which is governed, in addition to universal law, by norms issued by the Diocesan Bishop and in which the

Usage of Islamic Banking and Financial Services by United States Muslims

The Third Annual Conference of Islamic Economics & Islamic Finance Venue: Chestnut Conference Center, Toronto University, Canada Usage of Islamic Banking and Financial Services by United States Muslims

The Third Annual Conference of Islamic Economics & Islamic Finance Venue: Chestnut Conference Center, Toronto University, Canada Usage of Islamic Banking and Financial Services by United States Muslims

LONG ISLAND ABUNDANT LIFE CHURCH HICKSVILLE, NEW YORK. This church shall be known as the Long Island Abundant Life Church.

LONG ISLAND ABUNDANT LIFE CHURCH HICKSVILLE, NEW YORK "Grace be to you, and peace, from God our Father, and the Lord Jesus Christ." I Corinthians 1:3 We, the members of the Body of Christ, desiring that

LONG ISLAND ABUNDANT LIFE CHURCH HICKSVILLE, NEW YORK "Grace be to you, and peace, from God our Father, and the Lord Jesus Christ." I Corinthians 1:3 We, the members of the Body of Christ, desiring that

Church Profile. Prepared by the Polk Grove Settled Minister Search Committee 2017 POLK GROVE UNITED CHURCH OF CHRIST

Church Profile Prepared by the Polk Grove Settled Minister Search Committee 2017 POLK GROVE UNITED CHURCH OF CHRIST 9190 Frederick Pike Dayton, Ohio 45414 937.890.1821 www.facebook.com/polkgrove/ Part

Church Profile Prepared by the Polk Grove Settled Minister Search Committee 2017 POLK GROVE UNITED CHURCH OF CHRIST 9190 Frederick Pike Dayton, Ohio 45414 937.890.1821 www.facebook.com/polkgrove/ Part

The Board of Directors recommends this resolution be sent to a Committee of the General Synod. A Resolution of Witness

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 The Board of Directors recommends this resolution be sent to a Committee

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 The Board of Directors recommends this resolution be sent to a Committee

GLOBAL SURVEY ON THE AWARENESS AND IMPORTANCE OF ISLAMIC FINANCIAL POLICY

05 GLOBAL SURVEY ON THE AWARENESS AND IMPORTANCE OF ISLAMIC FINANCIAL POLICY The presence of an appropriate regulatory framework supported by financial policy is vital for an enabling environment that

05 GLOBAL SURVEY ON THE AWARENESS AND IMPORTANCE OF ISLAMIC FINANCIAL POLICY The presence of an appropriate regulatory framework supported by financial policy is vital for an enabling environment that

Islamic Banking Foundation Course Information Pack

Islamic Finance Institute of Southern Africa FOUNDATION COURSE IN ISLAMIC BANKING 4 Month Part-Time via Distance Learning Course Semesters : The 4 month Foundation Course in Islamic Banking takes place

Islamic Finance Institute of Southern Africa FOUNDATION COURSE IN ISLAMIC BANKING 4 Month Part-Time via Distance Learning Course Semesters : The 4 month Foundation Course in Islamic Banking takes place

4th ICIB Ministry of Planning Development & Reform Conference Secretariat: Mr. Ikram Ullah Khan Mr. Ehtesham Rashid

ICIB 4 th International Conference on Islamic Business 2016 Quaid-e-Azam Auditorium, IIUI Faisal Masjid Campus, Islamabad, Pakistan 20-22 February, 2016 Organized By: riphah international university riphah

ICIB 4 th International Conference on Islamic Business 2016 Quaid-e-Azam Auditorium, IIUI Faisal Masjid Campus, Islamabad, Pakistan 20-22 February, 2016 Organized By: riphah international university riphah

Does your church know its neighbours?

Does your church know its neighbours? A Community Opportunity Scan will help a church experience God at work in the community and discover how it might join Him. Is your church involved in loving its neighbours?

Does your church know its neighbours? A Community Opportunity Scan will help a church experience God at work in the community and discover how it might join Him. Is your church involved in loving its neighbours?

Endowment Fund Charter

Endowment Fund Charter Legal name of church, full address, (hereafter referred to as the Church ) hereby creates a permanent Endowment Fund to be known as the Name of the Church Endowment Fund (hereafter

Endowment Fund Charter Legal name of church, full address, (hereafter referred to as the Church ) hereby creates a permanent Endowment Fund to be known as the Name of the Church Endowment Fund (hereafter

Product Branding and Market Development Global Growth Opportunities. Daud Vicary Abdullah

Product Branding and Market Development Global Growth Opportunities Daud Vicary Abdullah 1 Agenda Facts and Figures Spreading the Word About Islamic Finance Opportunities Challenges to Development 2 What

Product Branding and Market Development Global Growth Opportunities Daud Vicary Abdullah 1 Agenda Facts and Figures Spreading the Word About Islamic Finance Opportunities Challenges to Development 2 What

Islamic Law of Property LAB2033 DR. ZULKIFLI HASAN

Islamic Law of Property LAB2033 DR. ZULKIFLI HASAN Contents Administration of Zakat Regulation on Zakat Management of zakah During the Prophet s s time Prophet appointed officer to collect and distribute

Islamic Law of Property LAB2033 DR. ZULKIFLI HASAN Contents Administration of Zakat Regulation on Zakat Management of zakah During the Prophet s s time Prophet appointed officer to collect and distribute

Regulatory Framework on Sharia-based Fintech: Current Issues

Regulatory Framework on Sharia-based Fintech: Current Issues Prof. Dato Dr Azmi Omar President & Chief Executive Officer 4 July 2018 INCEIF 2017 A member of AACSB INCEIF 2018 International Centre for Education

Regulatory Framework on Sharia-based Fintech: Current Issues Prof. Dato Dr Azmi Omar President & Chief Executive Officer 4 July 2018 INCEIF 2017 A member of AACSB INCEIF 2018 International Centre for Education

ALL AFRICA CONFERENCE OF CHURCHES (AACC) THE POST-JUBILEE ASSEMBLY PROGRAMMATIC THRUSTS (REVISED)

THE POST-JUBILEE ASSEMBLY PROGRAMMATIC THRUSTS (REVISED)") ALL AFRICA CONFERENCE OF CHURCHES (AACC) THE POST-JUBILEE ASSEMBLY PROGRAMMATIC THRUSTS 2014 2018 (REVISED) THE POST-JUBILEE PROGRAMMATIC THRUSTS 2014 2018 (REVISED) Table of CONTENTS INTRODUCTION... 4

ALL AFRICA CONFERENCE OF CHURCHES (AACC) THE POST-JUBILEE ASSEMBLY PROGRAMMATIC THRUSTS 2014 2018 (REVISED) THE POST-JUBILEE PROGRAMMATIC THRUSTS 2014 2018 (REVISED) Table of CONTENTS INTRODUCTION... 4

Welfare and Standard of Living

Welfare and Standard of Living Extent of poverty Marital status Households Monthly expenditure on consumption Ownership of durable goods Housing density Welfare and Standard of Living Extent of Poverty

Welfare and Standard of Living Extent of poverty Marital status Households Monthly expenditure on consumption Ownership of durable goods Housing density Welfare and Standard of Living Extent of Poverty

Shariah-Compliant Investments: Risks and Returns

Shariah-Compliant Investments: Risks and Returns BADLISYAH ABDUL GHANI CEO, Group Islamic Banking, CIMB Group CEO, CIMB Islamic Bank Bhd 2nd Islamic Wealth Management and Financial Planning Conference

Shariah-Compliant Investments: Risks and Returns BADLISYAH ABDUL GHANI CEO, Group Islamic Banking, CIMB Group CEO, CIMB Islamic Bank Bhd 2nd Islamic Wealth Management and Financial Planning Conference

POLICIES FOR LAUNCHING A MULTI-SITE FAITH COMMUNITY

POLICIES FOR LAUNCHING A MULTI-SITE FAITH COMMUNITY (MOTHER/DAUGHTER OR EXTENSION CAMPUS) When an established healthy church feels called by God to start a new congregation as a way of reaching a new mission

POLICIES FOR LAUNCHING A MULTI-SITE FAITH COMMUNITY (MOTHER/DAUGHTER OR EXTENSION CAMPUS) When an established healthy church feels called by God to start a new congregation as a way of reaching a new mission

Frequently Asked Questions for Incoming Churches Joining Foursquare via the Covenant Agreement

Frequently Asked Questions for Incoming Churches Joining Foursquare via the Covenant Agreement 1. What does it mean to be a fully Foursquare covenant church? The local church will be considered a Foursquare

Frequently Asked Questions for Incoming Churches Joining Foursquare via the Covenant Agreement 1. What does it mean to be a fully Foursquare covenant church? The local church will be considered a Foursquare

INTERIM REPORT OIC-STATCOM TECHNICAL COMMITTEE OF EXPERTS (TCE) ON ISLAMIC BANKING AND FINANCE STATISTICS

ON ISLAMIC BANKING AND FINANCE STATISTICS") INTERIM REPORT OIC-STATCOM TECHNICAL COMMITTEE OF EXPERTS (TCE) ON ISLAMIC BANKING AND FINANCE STATISTICS COUNTRY MEMBERS: Afghanistan, Azerbaijan, Bangladesh, Comoros, Egypt, Gambia, Iran, Jordan, Kazakhstan,